Editor’s Note: Updated with a tighter checklist, DSCR math, eligibility notes, and a realistic closing timeline.

Applying for a SBA loan can feel complex, but a clear checklist makes it manageable. This guide walks you through eligibility, documents, timelines, and DSCR so you can apply with confidence.

Key Terms (Glossary)

Applying for a SBA Loan: Step-by-Step Checklist

Applying for a SBA Loan: Eligibility & Fit

SBA programs fit different needs. Therefore, match the program to your use of funds. If you need working capital or mixed uses, 7(a) often fits well. If the anchor is real estate or large equipment, 504 may be stronger.

Want a quick side-by-side? See SBA 7(a) vs 504: Pick the Right Loan. It compares structure, equity, fees, and timelines. Use it to choose a path before you apply.

What Lenders Test First: DSCR and Cash Flow

Lenders underwrite repayment ability. They focus on DSCR and stable margins. They also review global cash flow when affiliates exist.

DSCR = Cash flow available for debt ÷ Annual debt service

Example: Cash flow equals $300,000. Annual debt service equals $200,000. DSCR equals 1.50. Coverage looks healthy at that level. However, stress test a 10% revenue dip before proceeding.

Get the basics here: DSCR for Small Businesses. It shows how to model coverage before applying for an SBA loan.

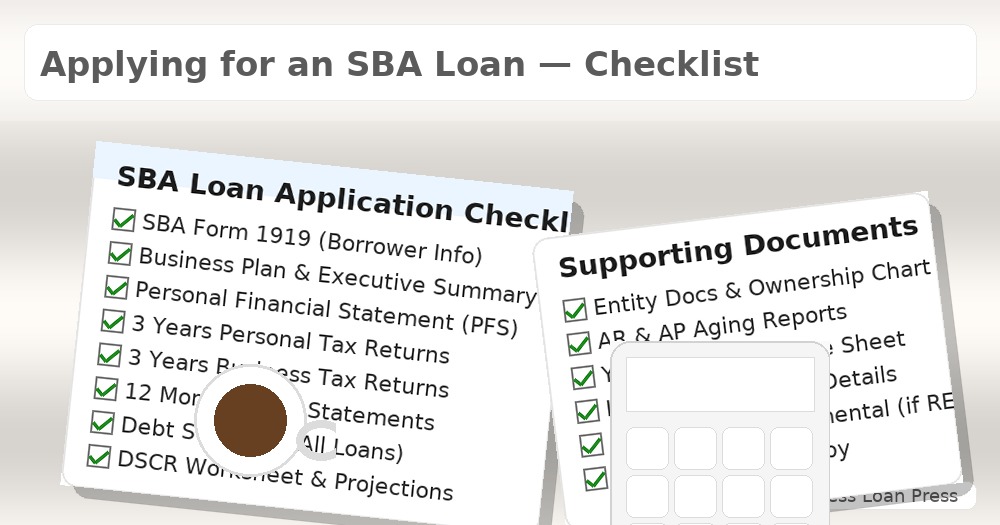

Documents to Gather Before Applying for a SBA Loan

- Three years business tax returns and K-1s.

- Three years personal tax returns for guarantors.

- YTD P&L, balance sheet, and prior year comparison.

- Trailing twelve months (TTM), if available.

- Debt schedule and last three bank statements.

- AR/AP agings and major contracts or leases.

- Purchase contract, quotes, or invoices for use of funds.

- Business plan summary and realistic projections.

- Personal financial statement for each guarantor.

Expect a 90–180 day bank statements underwriting review. Clean deposits, stable balances, and low NSF history help.

Step-by-Step: How to Apply with Confidence

- Define the use of funds. State the problem to solve first. Then align program fit.

- Model DSCR. Confirm coverage today and under mild stress. Adjust loan size if thin.

- Organize documents. Use the checklist above. Name files clearly for speed.

- Compare 7(a) and 504. Read the 7(a) vs 504 chooser. Select the path that supports cash flow.

- Request term sheets. Compare rate style, equity, fees, and prepayment rules.

- Open underwriting. Respond fast to conditions. Keep email updates short and clear.

- Order third-party reports. Appraisal, environmental, and title work drive timing.

- Finalize insurance and entity docs. Do this early. Surprises slow closings.

- Close and fund. Calendar covenant dates. Then track coverage quarterly.

Rates, Fees, and the True Cost Over Time

Sticker rate does not tell the whole story. Instead, amortize fees across the term for a fair view. Then compare total cost under realistic scenarios.

7(a) rates often float with an index. That can help if rates fall. However, rising rates raise payment risk. 504 fixes the CDC debenture. The bank piece may still float.

Model prepayment rules as well. You can avoid surprises later. Use a timeline that matches your plan to refinance or exit.

Collateral, Guarantees, and Equity

Collateral supports the file but does not replace cash flow. 7(a) uses available collateral where practical. 504 splits liens between bank and CDC.

Guarantees are standard above certain ownership levels. Equity varies by risk and use of funds. Begin planning that injection right away.

Check for filings that block closing. Learn how to find and remove UCC liens before you apply.

Timeline and Milestones

Strong files close faster. Therefore, front-load documents and quick answers. Clear use of funds reduces follow-up questions.

- Define structure and target loan size.

- Deliver core financials and projections.

- Align terms and assumptions in writing.

- Open underwriting and clear conditions.

- Order appraisal, environmental, and title.

- Complete insurance binds and entity items.

- Close, fund, and start reporting cadence.

Common Pitfalls When Applying for a SBA Loan

- Thin DSCR. Right-size the loan or add equity to protect coverage.

- Messy deposits. Clean flows three months before you apply.

- Gaps in documents. Missing K-1s and PFS forms cause delays.

- Unclear use of funds. Vague plans create more questions.

- Ignored covenants. Note reporting dates in your calendar now.

Helpful SBA resources:

Applying for a SBA Loan: FAQs

How much equity do I need? 504 commonly needs 10% or more. 7(a) varies with risk and use of funds.

Are there prepayment penalties? 504 has a declining debenture penalty. 7(a) can include penalties on longer terms.

Can I refinance short-term debt? Often yes under 7(a). Show a clear cash flow benefit and eligibility.

Will collateral gaps kill approval? Not always. Cash flow leads decisions. Collateral supports the file.

Next Steps

- Calculate coverage now with our DSCR explainer.

- Compare programs with the 7(a) vs 504 chooser.

- Clean deposits and inflows before applying for an SBA loan. See bank statements underwriting.

- Weigh lifetime cost. Review equipment financing vs leasing.

Image credit: Business Loan Press Studio. Feature Image Courtesy of Dreamstime.com

{kind=link}