Editor’s Note: Updated with deeper cost modeling, DSCR math, eligibility notes, and a step-by-step closing timeline.

Choosing between SBA 7(a) and SBA 504 shapes cash flow for years. Each program solves different problems. Therefore, the best choice depends on the use of funds and the associated risk. This guide explains trade-offs in plain English.

Key Terms (Glossary)

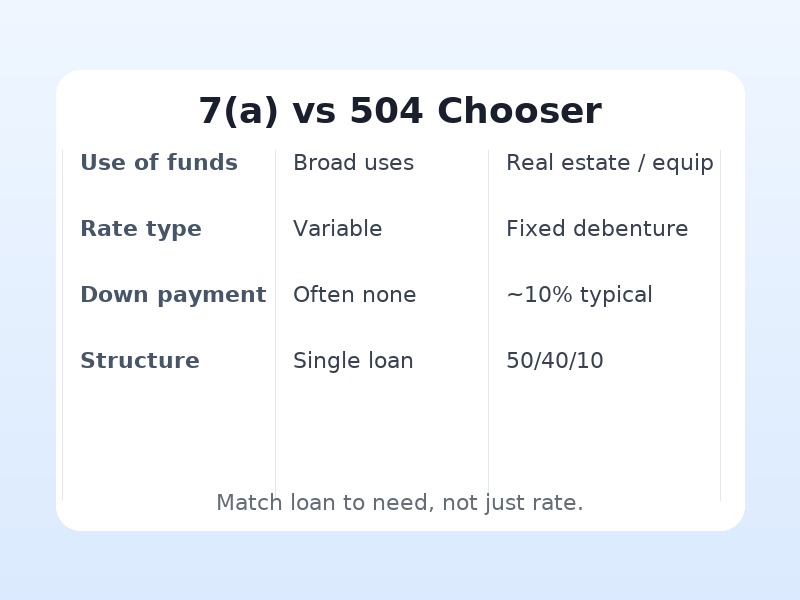

Start with use of funds, then compare rate style, structure, equity, and timeline.

Start with use of funds, then compare rate style, structure, equity, and timeline.Quick Chooser: What Fits Your Deal?

Begin with the problem you must solve. Then match the program to that problem. Finally, confirm structure and timing fit your plan.

| Dimension | 7(a) | 504 |

|---|---|---|

| Best for | Working capital, refi, mixed uses | Owner-occupied real estate, large equipment |

| Rate style | Usually variable | Fixed debenture component |

| Structure | Single loan | Bank 50% • CDC 40% • You 10%+ |

| Down payment | Often $0–10%, risk dependent | Commonly 10%+ equity |

| Speed | One lender, fewer steps | Two parties, more coordination |

| Flexibility | High for blended uses | Focused on fixed assets |

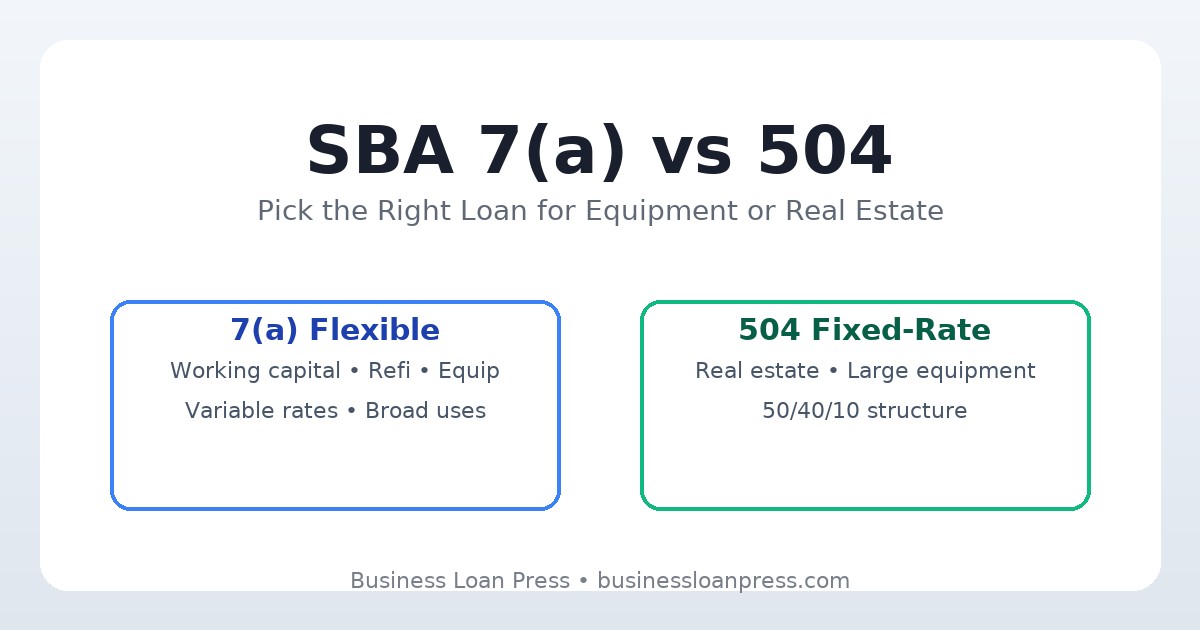

SBA 7(a) at a Glance

The 7(a) program favors flexibility. It can combine several needs in one facility. Typical uses include working capital, equipment, and refinancing. Real estate may appear in the mix as well.

Rates are usually variable. Terms can extend beyond conventional offers. Fees exist but spread over years. Underwriting emphasizes cash flow and guarantor strength.

SBA 504 at a Glance

The 504 program centers on fixed assets. That means owner-occupied property and heavy equipment. The structure uses a bank, a CDC, and your equity. Consequently, bank risk falls on large projects.

The CDC portion carries a fixed debenture rate. Terms are long for that piece. Fees are financed into the debenture. Underwriting focuses on project stability and occupancy.

Eligibility and Use of Funds

Both programs require for-profit, eligible businesses. Size standards apply across industries. Ownership and affiliate rules also matter. Talk structure early to prevent surprises.

Use of funds drives fit. Choose 7(a) when needs are blended or working-capital heavy. Choose 504 when the anchor is real estate or machinery. Mixed projects can split if needed.

Rates, Fees, and the True Cost

Sticker rate rarely tells the full story. Instead, model the total cost over time. Include fees, terms, and prepayment rules. Then test scenarios before deciding.

7(a) often floats with market indexes. That can help when rates fall. However, rising rates raise payment risk. 504 fixes the CDC slice for stability. Bank portions may still vary.

Amortize fees into the life of the loan. That yields a fair comparison. Next, include closing costs and interim interest. Finally, view monthly impact on cash flow.

Prepayment, Refinance, and Exit

Prepayment rules affect strategy. 504 has a declining penalty on the debenture. 7(a) can include penalties on longer maturities. Read this section before you sign.

Refinance goals also matter. 7(a) often handles refi plus working capital. 504 can refinance eligible fixed assets. Pick the path that clears the real constraint.

Speed and Certainty of Close

Speed depends on file quality. Clean financials accelerate both programs. Clear use of funds also reduces questions. Good communication keeps momentum.

7(a) uses one primary lender. Therefore, steps can compress. 504 adds a CDC partner and debenture funding. As a result, coordination takes longer.

Approval Math: DSCR and Global Cash Flow

Lenders test repayment strength with DSCR. The formula is simple and reliable. Stronger coverage increases approval confidence. Thin coverage invites deeper review.

DSCR = Cash flow available for debt ÷ Annual debt service

Underwriting may “global” results. That means they include related entities and guarantor debts. Consistent margins support approval. Predictable revenue helps as well.

Example: Suppose cash flow available equals $300,000. Annual debt service equals $200,000. DSCR equals 1.50. Coverage looks healthy at that level. Stress test with a 10% revenue dip, too.

Collateral, Guarantees, and Equity

Collateral strengthens files but does not replace cash flow. 7(a) uses available collateral where practical. 504 places first on the bank portion. The CDC holds its own lien as well.

Personal guarantees are standard. Ownership thresholds trigger guarantees. Equity varies by risk and use. Start planning that injection early.

Three Real Scenarios

Owner-occupied building purchase: 504 often wins here. The fixed CDC piece lowers rate risk. Bank risk falls with a first lien. Your equity supports the stack.

Heavy equipment plus working capital: 7(a) usually fits. You can combine soft costs and equipment. You can also refinance higher-rate debt. Cash flow relief improves flexibility.

Refinance with expansion: Both programs can work. 7(a) handles mixed uses smoothly. 504 may fit if property is the anchor. Choose after modeling total cost.

Documentation Checklist

- Three years business tax returns and K-1s

- Three years personal tax returns for guarantors

- Year-to-date P&L and balance sheet

- Prior year comparison and trailing twelve months

- Debt schedule and recent bank statements

- AR/AP agings and key contracts or leases

- Purchase contract, invoices, or equipment quotes

- Business plan summary and realistic projections

- Personal financial statement for each guarantor

Timeline and Milestones

Strong files close faster. Therefore, front-load documents and responses. Track tasks weekly until close. Confirm third-party orders in writing.

- Define use of funds and target structure.

- Gather core financials and projections.

- Receive a term sheet and align assumptions.

- Open underwriting and clear conditions promptly.

- Order appraisal, environmental, and title work.

- Finalize entity docs and insurance quotes.

- Close, fund, and calendar any covenants.

Risk Controls and Covenants

Expect standard insurance and reporting covenants. Provide statements on a regular cadence. Keep taxes current at all times. Proactive updates preserve trust.

Growth plans should match projections. Material changes belong in early emails. Lenders appreciate early signals. Clarity keeps relationships healthy.

Decision Flow: 7(a) or 504?

- Is the anchor asset real estate or heavy equipment? If yes, weigh 504 first.

- Do you need working capital or blended uses? If yes, consider 7(a).

- Is fixed-rate stability a priority? If yes, the 504 debenture helps.

- Do you want fewer steps and parties? If yes, 7(a) may be faster.

- Model DSCR and total cost. Choose the stronger cash flow outcome.

Frequently Asked Questions

How much equity do I need? 504 commonly needs 10% or more. 7(a) varies with risk and purpose. Confirm early to avoid delays.

Can I include tenant income with 504? Limited tenant income can be allowed. Owner-occupancy rules still apply. Discuss structure with your lender.

Are there prepayment penalties? 504 has a declining debenture penalty. 7(a) may include penalties on longer terms. Model the effect before closing.

Can I refinance short-term debt? Often yes under 7(a). The refinance must meet program rules. Provide a clear cash flow benefit.

Will collateral gaps kill approval? Not always. Cash flow coverage leads decisions. Collateral supports but rarely replaces DSCR.

Next Steps

- Calculate coverage today. Read our DSCR explainer.

- Check for filings that block closing. See our UCC guide.

- Clean deposits and inflows. Learn what underwriters see.

- Compare total cost over time. Review equipment options.

Use the chooser to align program, structure, and cash flow goals.

Use the chooser to align program, structure, and cash flow goals.Image credit: Business Loan Press Studio.

vs 504: Pick the Right Loan for Equipment or Real Estate){kind=link}