Small business owners often need extra funding to grow or survive. Grants and loans are two common options. Grants sound appealing because they do not require repayment. Loans are reliable but come with debt obligations.

What Is a Small Business Grant?

A grant provides funds to a business without repayment. Federal, state, or private organizations may offer them. Grants usually focus on specific industries, demographics, or projects. Applying requires careful attention to eligibility and application details.

Grants can support innovation, community projects, or minority-owned businesses. Winning a grant means extra cash without future debt. However, competition is fierce. Many applicants compete for limited funds.

What Is a Small Business Loan?

A loan provides a lump sum or line of credit that must be repaid. Repayment includes interest and fees. Banks, credit unions, online lenders, and the SBA offer loans. Approval often depends on credit history, revenue, and collateral.

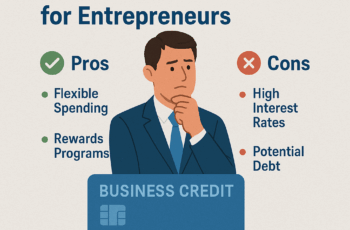

Loans are flexible. You can use them for equipment, expansion, or working capital. Unlike grants, loans are generally easier to find. But loans add debt to your balance sheet.

The Appeal of Free Money

Grants feel like “free money” because no repayment is required. They support projects without draining future cash flow. Winning a grant can also enhance reputation. It shows recognition from trusted organizations.

However, grants usually have strict conditions. Funds may only cover certain expenses. You must report how the money is used. Failing to meet requirements risks losing funding or facing penalties.

The Reliability of Loans

Loans are predictable. Approval brings a clear repayment schedule. You know your costs and obligations upfront. That reliability allows for structured planning.

Loans can be larger than most grants. You can often secure higher amounts to fund major projects. But repayment continues even if revenue dips. That pressure can strain cash flow in slow months.

Application Processes Compared

Applying for a grant is lengthy. You must prepare proposals, budgets, and supporting documents. Deadlines are strict and competition is heavy. Decisions may take months.

Loan applications also require paperwork but are often faster. Banks may take weeks. Online lenders may respond within days. You usually need financial statements, tax returns, and credit information.

Approval Odds

Grants are very competitive. Approval odds can be slim due to high demand. Many excellent businesses never receive awards. Winning often requires professional grant writing or consulting help.

Loan approvals vary by credit and collateral. Strong credit improves odds. Even businesses with weaker credit may qualify through online lenders, though at higher costs. While not guaranteed, loans are more widely accessible than grants.

Restrictions on Use

Grants are often tied to specific purposes. A grant for research cannot pay for marketing. A grant for hiring may not cover equipment. Flexibility is limited.

Loans generally allow broader use. Funds can cover operating costs, payroll, expansion, or new projects. Lenders may ask about your plans but rarely restrict categories. This makes loans more adaptable.

Costs of Funding

Grants have no repayment or interest. The main cost is time and effort spent applying. That opportunity cost can be high. Professional grant writing services also charge fees.

Loans require repayment with interest. Total costs depend on the rate and term. Short-term loans may carry high APRs. SBA loans usually offer lower rates and longer terms.

Impact on Cash Flow

Grants do not affect future cash flow directly. Once awarded, funds are yours. This makes them attractive for businesses needing a cash boost without repayment stress. However, late or denied applications leave gaps.

Loans require consistent repayment. Cash flow planning must account for monthly obligations. Defaulting on payments damages credit and risks asset seizure. Predictability helps budgeting but increases financial pressure.

Risks and Responsibilities

Grants carry compliance risks. You must follow strict guidelines on how funds are used. Audits may occur. Misuse can require repayment or legal consequences.

Loans carry debt risks. Falling behind on payments harms your credit and reputation. Collateral can be seized. Personal guarantees may affect your personal finances. The risk grows if sales underperform expectations.

Who Should Choose Grants?

Grants suit businesses meeting eligibility criteria. Nonprofits, startups in targeted industries, and minority-owned companies may qualify. Businesses with time to complete lengthy applications also benefit. Patience and strong proposals are key.

Grants are ideal for projects with public or community benefit. They are also best when repayment would burden the business. For example, research initiatives or environmental projects often align with grant goals.

Who Should Choose Loans?

Loans suit businesses needing immediate, flexible funding. They fit companies planning expansion, buying equipment, or managing working capital. Businesses with strong credit gain access to better rates and terms. Loans also fit entrepreneurs who value speed.

If your business cannot wait months for funding decisions, loans make sense. They allow faster action on opportunities. For companies prepared to manage debt responsibly, loans provide reliability.

Decision Checklist

- Do you meet grant eligibility requirements?

- Can you handle the lengthy grant process?

- Is your business credit strong enough for loans?

- Do you need flexible funding or restricted use?

- Can your cash flow support loan repayment?

- Are you willing to take on debt?

Bottom Line

Grants and loans both provide small business funding. Grants offer free money but come with fierce competition and restrictions. Loans offer reliable funding but require repayment and add debt. Choosing wisely means weighing eligibility, urgency, cash flow, and goals. Match the funding source to your business strategy for long-term success.

Sources

- U.S. Small Business Administration – Small Business Grant and Loan Resources.

- Grants.gov – Federal Grant Database and Application Guide.

- National Federation of Independent Business – Reports on small business financing challenges.

- Federal Reserve Banks, Small Business Credit Survey.

- Investopedia and Forbes articles on grants versus loans.

Feature image created in collaboration with DALL-e

{kind=link}