Editor’s Note: This article was originally published in 2021 and updated in September 2025. It has been expanded with additional insights, examples, and preparation strategies to help business owners make smarter borrowing decisions.

Applying for a small business loan can feel overwhelming. Lenders advertise endless options, and it is easy to get lost in the fine print. Choosing the wrong loan may create cash flow challenges, strain your personal finances, or even stall growth.

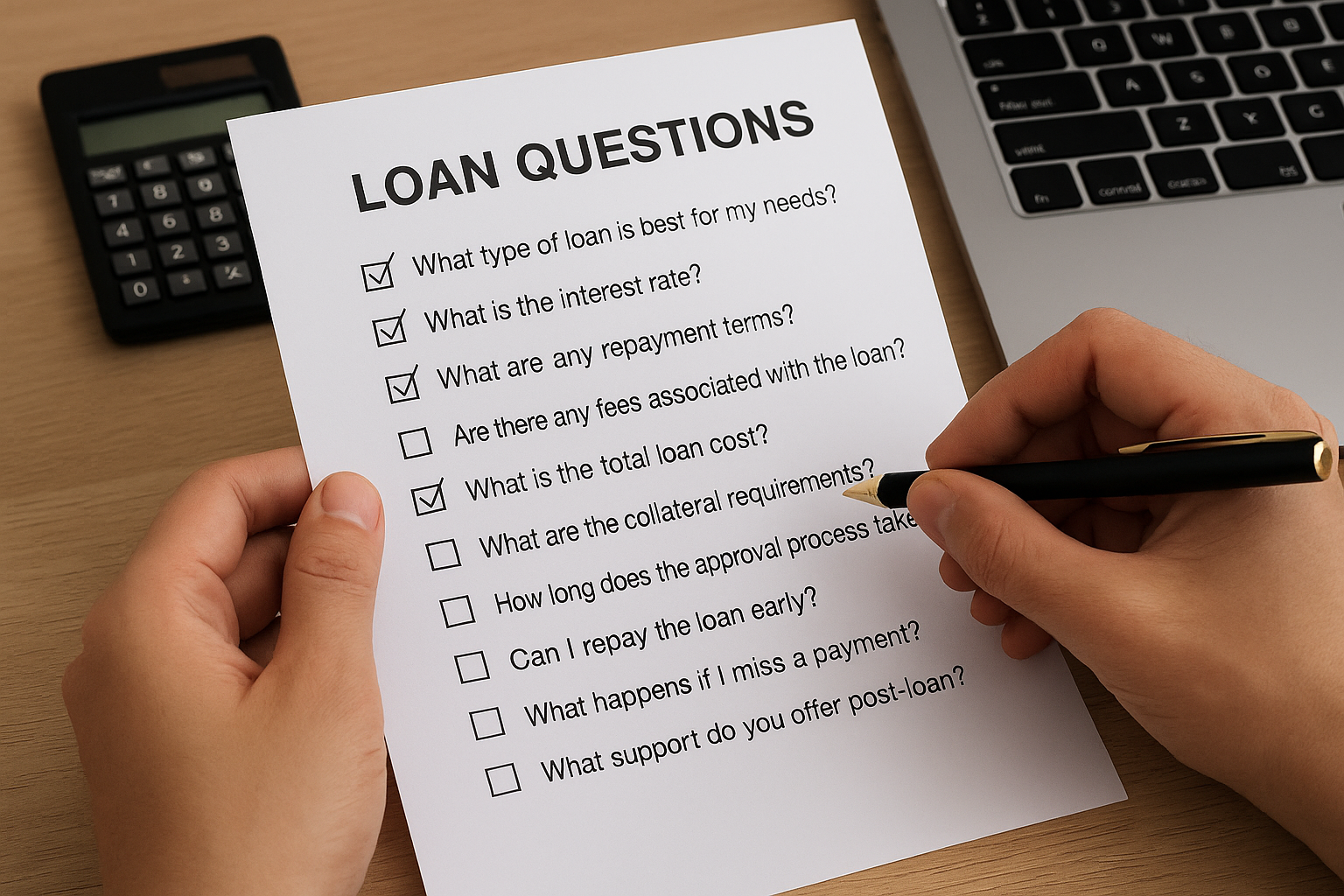

Asking clear, targeted questions reduces risk, reveals hidden costs, and positions you for approval. This article highlights ten essential questions every borrower should ask, explains common mistakes, and shows how to prepare for lender meetings.

Why Asking Questions Matters

Lenders are not just evaluating your business; they are also evaluating how prepared you are. Business owners who ask focused questions appear more professional and reduce the likelihood of costly misunderstandings.

These questions also create opportunities to negotiate better terms. Borrowers who take time to clarify details often walk away with lower fees, improved flexibility, and stronger lender relationships.

Common Mistakes Borrowers Make

One frequent mistake is focusing only on approval speed instead of overall cost. For example, online lenders may provide funding within 48 hours but charge interest rates twice as high as traditional banks. Another mistake is underestimating the impact of collateral requirements.

Losing equipment or property because of a default can cripple operations. Borrowers also fail to consider prepayment penalties, which can punish businesses that grow faster than expected. Avoiding these errors can save your company thousands of dollars and protect long-term stability.

1. What Type of Loan Is Best for My Needs?

Each loan type serves a distinct purpose. Term loans, SBA-backed loans, merchant cash advances, and lines of credit all operate differently. For example, a line of credit may suit seasonal businesses needing flexible access to funds. A term loan may be better for purchasing equipment or real estate. Asking this question ensures the product aligns with your cash flow and growth goals.

2. What Is the Interest Rate?

The interest rate significantly influences repayment affordability. A seemingly small difference—8% versus 10%—adds up over several years. Clarify whether your rate is fixed or variable.

A fixed rate guarantees stable payments, while a variable rate may increase as markets shift. Business owners who fail to ask may face sudden spikes in repayment amounts. See more about fixed versus variable loans.

3. What Are the Repayment Terms?

Repayment terms are more than just the loan length. Ask about payment frequency, grace periods, and options for restructuring if revenue falls short. Daily or weekly payments may overwhelm businesses with uneven cash flow, even when the loan amount seems manageable. Using a business loan calculator allows you to test scenarios before committing.

4. Are There Any Fees Associated with the Loan?

Lenders often charge fees in addition to interest. These may include origination, application, underwriting, and servicing fees. Some also charge penalties for early payoff or missed payments. A loan with a low interest rate but high fees can cost more than one with a slightly higher rate. Always request a written fee schedule. Our guide on hidden loan fees explains what to watch for.

5. What Is the Total Loan Cost?

Total cost equals the principal plus all interest and fees over time. This number reveals the true price of borrowing. Request an amortization schedule and compare total costs across different lenders. A business that borrows $100,000 at 8% for ten years will repay nearly $150,000. Understanding this figure helps you determine whether the loan is worth it.

6. What Are the Collateral Requirements?

Collateral secures the loan but puts assets at risk. Lenders may require real estate, vehicles, or personal guarantees. Consider whether you are comfortable pledging those items. Businesses that fail to ask about collateral sometimes discover too late that personal property is on the line. Review our article on collateral in small business loans for more insights.

7. How Long Does the Approval Process Take?

Approval speed often determines whether a business can seize opportunities. Traditional banks may take weeks, while online lenders sometimes approve within 24 hours. Ask not only about approval but also about funding times. Delays may leave you unable to pay suppliers or secure discounts. Learn more in our guide to loan approval timelines.

8. Can I Repay the Loan Early?

Some lenders welcome early repayment, while others add costly penalties. Businesses that grow quickly often want to clear debt sooner. Without asking, you may face unnecessary charges for doing so. Confirm whether early payoff is allowed without penalty. See our article on early repayment pros and cons.

9. What Happens If I Miss a Payment?

No business plans to miss payments, but emergencies happen. Ask about late fees, grace periods, and whether missed payments are reported to credit agencies. A single missed payment can damage your credit score and increase future borrowing costs. Understanding the consequences helps you prepare for potential setbacks.

10. What Support Do You Offer Post-Loan?

Some lenders provide ongoing support through account managers or financial advisors. This guidance can help you manage debt and plan future financing. Others simply process payments and leave borrowers on their own. Asking ensures you know whether the relationship ends at funding or continues with ongoing assistance.

How to Prepare Before Meeting Your Lender

Strong preparation improves approval odds and may even lower your rate. Gather at least two years of tax returns, recent profit-and-loss statements, and updated cash flow projections. Lenders want evidence of consistent revenue and sound financial management.

Check your personal and business credit scores for errors before applying. Create a business plan that explains how you will use the funds. Preparation shows professionalism and strengthens your credibility with lenders.

Conclusion

Asking the right questions turns a confusing process into an informed decision. You gain clarity on costs, repayment, collateral, and lender expectations. Avoiding common mistakes and preparing strong documentation improves your approval chances.

Compare multiple lenders, negotiate when possible, and consider long-term impacts before signing. A little preparation now protects your finances and sets your business up for sustainable growth.

Sources

- U.S. Small Business Administration – Business Loans

- Investopedia – Questions Before Getting a Loan

- NerdWallet – Business Loan Guide

- Forbes – Questions Before Applying

- Fundera – Business Loan Questions

Photo credit: Featured and inline images AI-generated by ChatGPT for BusinessLoanPress.com.

{kind=link}