Year-End Small Business Money Checklist: Taxes, Cash Flow, and Clean Books Before January

Merry Christmas from Business Loan Press. This year-end small business money checklist is built for January execution and lender readiness. It prioritizes statement credibility, cash timing visibility, and tax documentation. Those three areas influence borrowing terms, vendor negotiations, and operating decisions.

A year-end close is a control exercise, not an administrative ritual. Reconciled balances convert reports from summaries into evidence. Timing analysis converts cash flow from a guess into a schedule. Together, they improve decisions and reduce avoidable rework during January.

Year-End Small Business Money Checklist: Statement credibility comes first

Start with reconciliations because every downstream metric depends on that base. Reconcile business checking and savings to bank statements, not only to feeds. Reconcile each business credit card to its statement balance. If balances do not match, profit and cash metrics are unreliable.

When mismatches appear, use a structured sequence to isolate causes. Check for duplicate imports, missing transactions, and incorrect transfer postings. Confirm statement cutoff dates, especially around month-end deposits and card charges. Document each correction with a brief note that explains the adjustment.

Do not skip payment processors because they often distort revenue timing. Reconcile Stripe, Square, PayPal, and ecommerce payouts to deposits and fees. Processor deposits are usually net of refunds, fees, and chargebacks. Without reconciliation, revenue lines can disagree with bank reality.

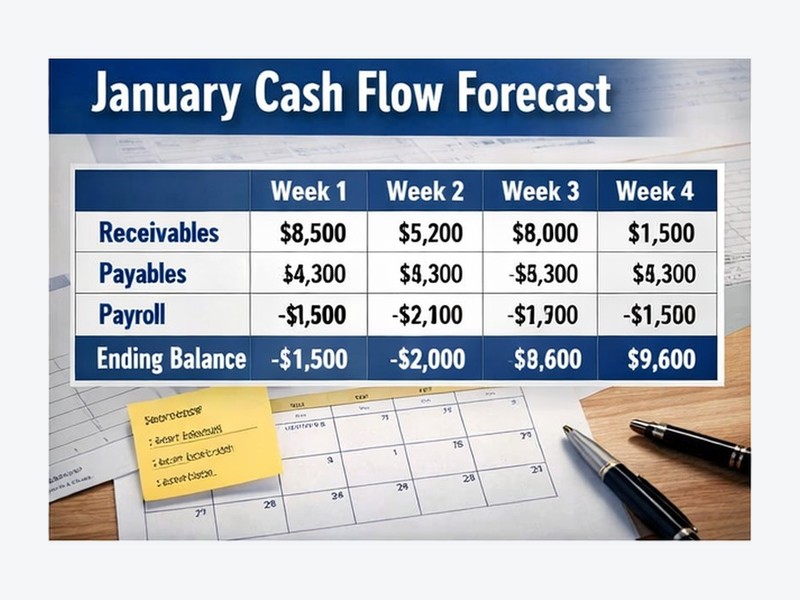

Cash flow timing: treat it like a calendar, not an average

Cash flow is a schedule of inflows and obligations, not a monthly average. Payroll has dates, debt has dates, rent has dates, and taxes have dates. Revenue also has dates, and those dates are often uneven. A useful close maps timing instead of assuming deposits will smooth out.

Begin with a simple January cash flow forecast built from known items. Use invoice due dates, contract billing dates, and expected processor payout timing. List payroll, rent, debt service, insurance, and key vendor payments by due date. The output should show weekly liquidity, not only monthly totals.

Receivables are a primary timing lever for many businesses. Review invoices by age and focus on the oldest balances first. Send reminders with invoice number, amount, and a payment link. If partial payment is required, confirm a two-part plan with specific dates.

Payables are the second timing lever, and terms matter more than intentions. Separate obligations into payroll-critical, operations-critical, and deferrable spending. Communicate early with vendors when timing gaps appear. Early term discussions preserve options and protect supplier relationships.

If you prefer a lender-aware forecasting method, use your internal guide. See Cash Flow Projections in Securing a Business Loan for a structured approach. It connects statements, collections, and timing assumptions. That connection improves credibility during financing discussions.

Working capital control: receivables, payables, and recurring costs

Working capital strength is largely policy-driven, not luck-driven. If receivables age without follow-up, operations fund customers. If collections are consistent, customers fund operations through timely payments. Use year-end to confirm that your policies match actual customer behavior.

Review subscription and recurring expenses with a performance lens. Recurring tools should earn their cost through time saved or revenue supported. Cancel low-use tools and duplicate services. Recurring costs compound quietly and tighten working capital throughout the year.

Debt schedules also require a year-end validation step. Confirm balances, interest rates, and autopay settings against statements. Verify that payment dates align with your revenue timing. If refinancing is a 2026 goal, clean documentation reduces underwriting back-and-forth.

Margin integrity: inventory, work-in-progress, and cost reality

Margin analysis depends on accurate cost assignment and accurate operational status. For product businesses, inventory errors misstate cost of goods and profit. For service businesses, untracked work-in-progress hides timing and profitability issues. Both problems weaken decision-making and lender confidence.

If you sell products, complete a defensible physical inventory count. Reconcile the count to records and adjust for shrink, damage, and obsolete stock. Obsolete stock inflates profit if it remains valued as sellable inventory. Accurate inventory produces margins that are comparable across months.

If you sell services, treat work-in-progress as your operational inventory. List open projects, expected billing dates, and scope changes. Scope changes often explain labor overruns that appear as expense spikes. When project timing is visible, staffing and cash scheduling become more precise.

Update meaningful cost changes before you set next-quarter pricing assumptions. Supplier increases, shipping changes, and labor shifts often move faster than price updates. Old costs create false margins and distort budgeting. Accurate costs support credible forecasts and stronger lender conversations.

Categories and statements: aim for readable trends, not perfect taxonomy

Category cleanup is valuable when it increases interpretability of trends. A profit and loss statement is a pattern tool, not a trophy. It works when categories are consistent across months. Consistency allows comparisons that support pricing, hiring, and spending decisions.

The categories that reduce interpretability are usually predictable. Meals, supplies, and subscriptions often become catch-alls. Catch-alls blur discretionary spending and operational spending. Reclassify enough transactions to make the monthly pattern clear and repeatable.

Once statements are readable, identify what is driving variance. Separate pricing issues from cost issues using gross margin and operating margin movement. Separate timing issues from profitability issues using cash flow and receivables changes. This diagnostic step is where year-end reporting becomes executive analysis.

Lender readiness: produce the package lenders expect to see

Export a year-end profit and loss statement and a year-end balance sheet as PDFs. Save a current debt schedule and a twelve-month bank statement set. Store these documents in a single “Year-End Reports” folder. The goal is fast retrieval when a lender requests support.

Lenders evaluate both capacity and discipline, and documentation signals discipline. If you want an underwriting checklist perspective, use your internal post. See Applying for A SBA Loan: What Lenders Look For for common documentation requests. If you are planning ahead, also review Small Business Loan Requirements 2025: The Complete Guide.

Speed is usually determined by completeness, not by persuasion. Missing documents slow underwriting because follow-up cycles are sequential. If timing is important next quarter, build readiness now. For process improvements, see From Application to Approval: How to Get Your Small Business Loan Faster.

Taxes and recordkeeping: treat documentation like risk management

Tax planning is most effective when it is linked to cash planning. The common failure is not the tax rate itself. The failure is reserving too little cash for known obligations. A year-end small business money checklist should include a reserve decision and a documentation routine.

If estimated taxes apply, confirm due dates with your tax professional. Verify whether state dates differ from federal dates. Reserve funds deliberately based on conservative assumptions. A reserve decision is easier when your reconciliations and forecasts are already credible.

Maintain a “Tax Packet” folder with statements, payroll summaries, year-end reports, and major receipts. Add a short notes file for unusual events, including large refunds or one-time equipment purchases. Notes reduce interpretation risk when reviewing deductions later. When retention rules are unclear, follow professional guidance and retain longer.

Final thoughts

This year-end small business money checklist is designed to produce decision-grade statements and an actionable January forecast. Reconciliations create credibility, timing analysis creates control, and margin accuracy creates pricing clarity. Those elements improve lender readiness and improve operating decisions. Merry Christmas from Business Loan Press, and best wishes for a strong start in January.

Sources

- IRS: Recordkeeping

- IRS: How long should I keep records?

- IRS: Estimated tax basics

- SBA: Manage your finances

- SCORE: Small business mentoring and resources

Financial Disclaimer: The information in this article is provided for general educational purposes only and should not be considered financial, legal, or tax advice. I am not acting as your financial advisor, attorney, or accountant, and no professional-client relationship is created by your use of this content. Laws, regulations, lender guidelines, and tax rules can change, and your circumstances may be different. Before making significant financial decisions or signing loan documents, consult qualified professionals who can evaluate your specific business, risks, and goals.

Photo Credit: All images © Sloan Digital Publishing and licensed stock sources. Used with permission.

{kind=link}