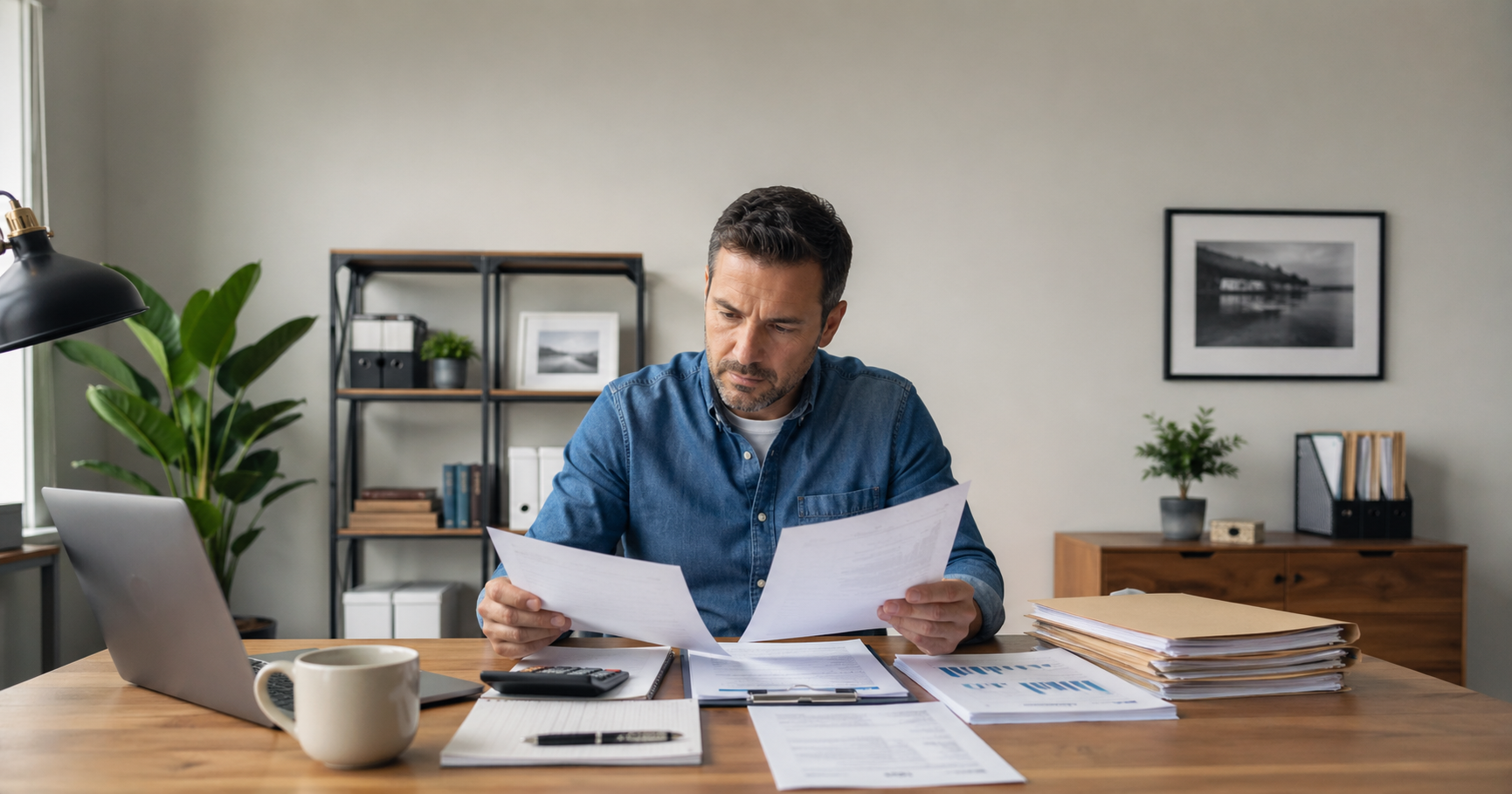

Pandemic loan collections are no longer a distant concern for some small business owners. Recent SBA action shows that old PPP and COVID EIDL issues can still resurface years later. For legitimate borrowers, the lesson is not panic. It is preparation, documentation, and a clear understanding of what collection activity may mean.

Many business owners accepted pandemic relief during an emergency. Some used the money properly and kept records. Others may have misunderstood repayment terms, forgiveness rules, or communication from lenders and agencies. A smaller group may have submitted false information or participated in fraud.

Those situations are very different, but they can all create anxiety when old loan files return. Business owners should understand the difference between ordinary repayment problems and serious fraud allegations. They should also know what records may help protect them.

Why Pandemic Loan Collections Are Back in the News

The Small Business Administration recently announced a major referral involving suspected pandemic-era loan fraud. The agency said it referred hundreds of thousands of suspected fraudulent loans to the Treasury Department for collection. The loans involved Paycheck Protection Program loans and COVID Economic Injury Disaster Loans.

This does not mean every pandemic borrower is in trouble. It also does not mean every delinquent borrower committed fraud. Business owners should avoid assuming the worst based on a headline. However, the announcement is a strong reminder that government-backed business loans can carry long-term obligations.

PPP and COVID EIDL were created during an unusual national emergency. Programs moved quickly because businesses needed help fast. That speed helped many employers survive. It also created confusion, recordkeeping problems, and opportunities for abuse.

For legitimate borrowers, the most useful takeaway is practical, especially when old debt affects broader small business debt management. Old loan paperwork, forgiveness records, payment histories, and business documents still need to be available. A forgotten file can become very important when a notice arrives.

What Pandemic Loan Collections Through Treasury May Mean

A Treasury collection referral generally means a debt has moved beyond ordinary servicing. The government may use federal collection tools to pursue repayment. These tools can include notices, collection letters, administrative offsets, and other lawful recovery methods.

The details can vary by loan type, balance, status, and borrower situation. A small business owner should read every notice carefully. Deadlines, contact instructions, appeal options, and payment directions may be included in the letter.

Ignoring a collection notice is usually the worst response. Silence can reduce options and increase costs. It can also make a correctable problem harder to solve. Even when a business owner believes the notice is wrong, the issue still needs a documented response.

Owners should also be cautious about scams. Government collection activity can attract fake callers, fake emails, and misleading payment demands. Any suspicious notice should be verified through official agency channels before money is sent.

Fraud Flags Are Different From Ordinary Repayment Problems

One important distinction deserves careful attention. A repayment problem is not always a fraud problem. Businesses can become delinquent for many reasons, including closure, cash flow collapse, confusion, or administrative mistakes.

Fraud involves something more serious. It may include false statements, fake businesses, identity theft, inflated payroll claims, or misuse of loan proceeds. Those allegations can carry civil and criminal consequences.

That difference is why documentation matters so much. A legitimate borrower may need records showing how funds were requested, received, used, forgiven, or repaid. Clear records help separate ordinary financial hardship from questionable activity.

Business owners should not try to explain complex loan concerns casually over the phone. Sensitive issues deserve careful review. If fraud, identity theft, or legal exposure is possible, qualified legal guidance is important.

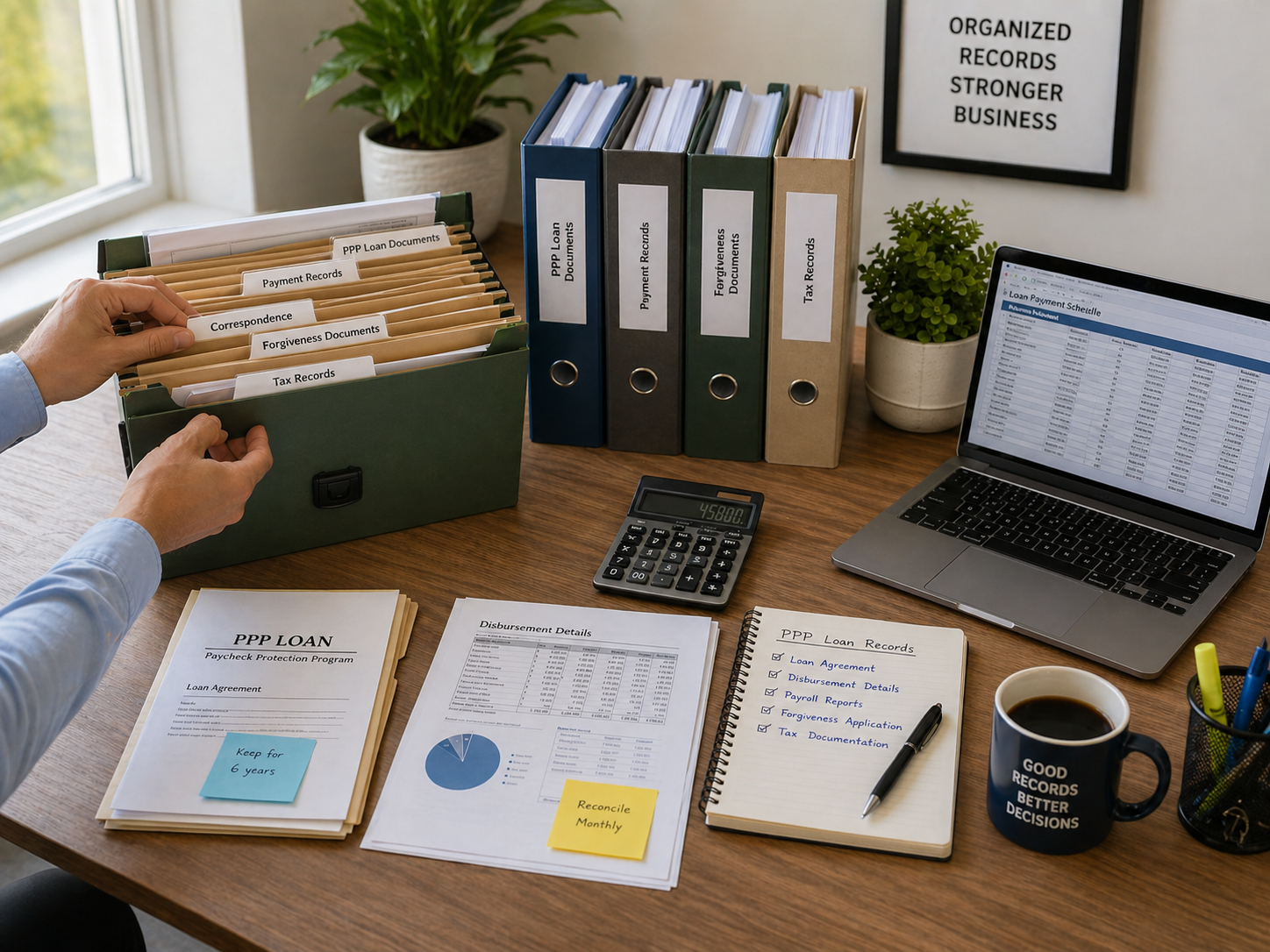

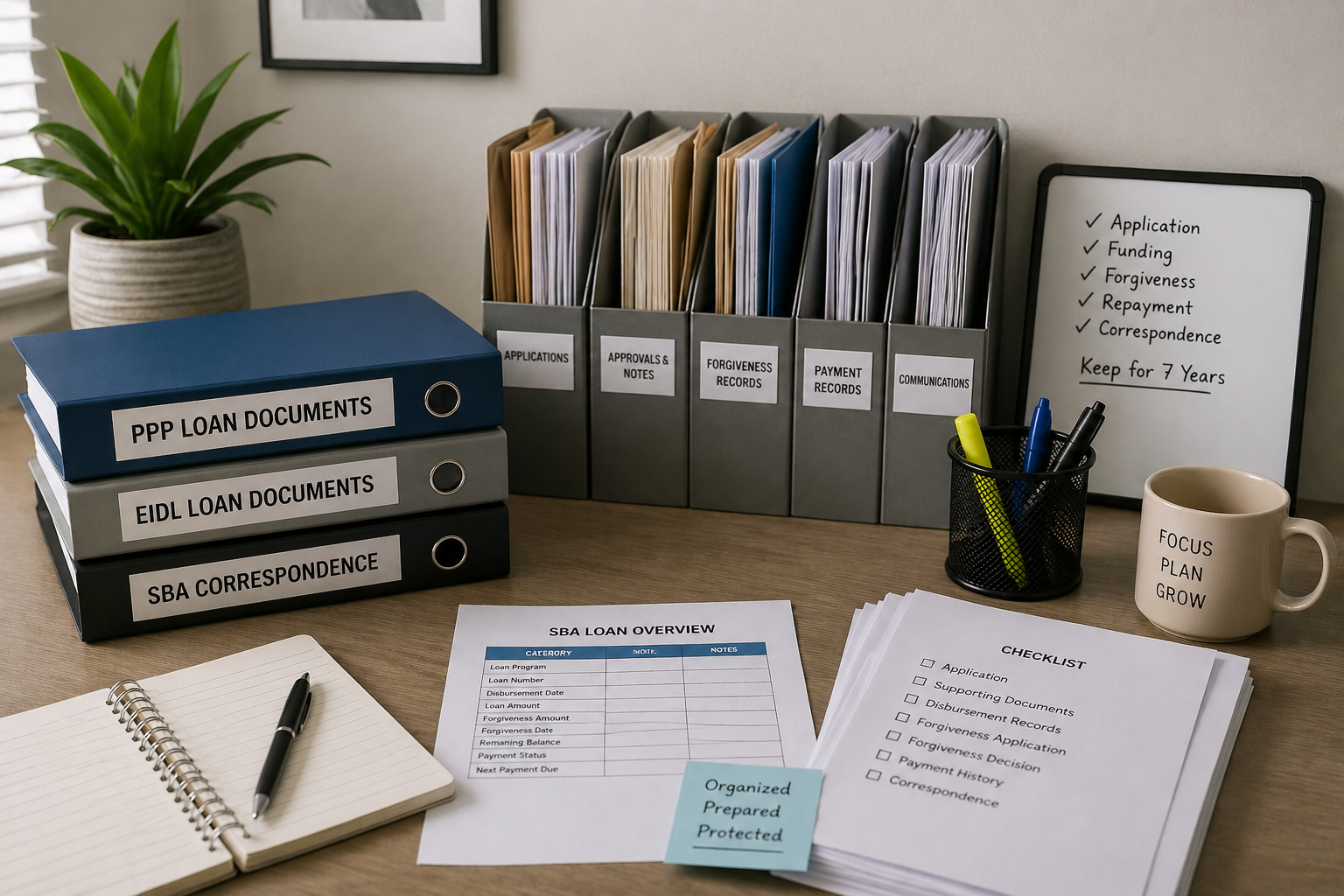

Records Business Owners Need for SBA Loan Collections

Many owners are not thinking about pandemic loan files anymore. That is understandable, but it can be risky. Pandemic loan collections show why older records still deserve organized storage.

Start with the original loan application, approval documents, and loan number. Keep copies of promissory notes, forgiveness applications, lender messages, SBA correspondence, and payment records. For EIDL loans, include repayment schedules and account statements.

Next, gather records showing how funds were used. These may include payroll reports, bank statements, rent payments, utility bills, vendor invoices, and tax records. The goal is to create a clear paper trail that supports stronger business loan documentation.

Owners should also keep proof of business activity during the loan period. Useful records may include licenses, payroll filings, sales records, insurance documents, and lease agreements. These documents can help verify that the business was real and operating.

Digital storage helps, but it should not be the only method. Keep backup copies in a secure location. Name files clearly, so they can be found quickly under stress.

What Legitimate Borrowers Should Do After Receiving a Notice

A collection notice should not be tossed aside or answered emotionally. The first step is to confirm the notice is real. Check the agency name, account details, contact instructions, and mailing address.

Next, compare the notice with your own records. Look at the loan number, balance, payment history, and any forgiveness decision. If something appears wrong, document the discrepancy before contacting anyone.

Then decide what type of help is needed. A bookkeeper may help organize records. A CPA may help review tax and payroll documents. An attorney may be needed if fraud allegations, identity theft, or personal liability concerns appear.

Business owners should keep written notes of all conversations. Record dates, names, reference numbers, and instructions received. Follow up in writing whenever possible.

Payment discussions should also be handled carefully. Do not agree to terms that cannot be met. A realistic repayment plan is better than a promise that fails quickly.

Why This Affects More Than Past Borrowers

Pandemic loan collections may also affect future borrowers. Fraud losses can make future emergency lending programs stricter. That can mean more paperwork, slower approvals, and stronger verification requirements.

Honest business owners often pay the price for widespread abuse. Lenders and agencies may become more cautious. That caution can delay funding for companies with real needs.

This is one reason program integrity matters to ordinary businesses. Fraud does not only harm taxpayers. It can damage trust in the entire small business lending system.

Stronger oversight can be frustrating, but it also protects legitimate borrowers. A cleaner lending system can preserve access to capital. It can also reduce unfair competition from businesses that obtained funds improperly.

How to Reduce Risk With Future Business Loans

Every business loan should be treated as a long-term financial file. Owners should understand the purpose, repayment terms, default rules, collateral requirements, and personal guarantee language before signing.

For government-backed loans, the paperwork may be especially important. Public programs often include eligibility rules, use restrictions, audit rights, and reporting obligations. These details should not be skimmed.

Before applying for a small business loan, owners should confirm that records match the application. Revenue, payroll, employee counts, ownership details, and tax filings should be consistent. Inconsistencies can create problems later.

After funding, the business should track how the money is used. Separate accounting categories can help. Clear records are easier to defend than reconstructed explanations years later.

Finally, business owners should ask questions before problems develop. Lenders, accountants, and attorneys can often prevent small errors from becoming expensive disputes.

Why Old SBA Loan Files Still Matter During Collections

Some business owners may feel safe because their loan was small. Others may assume that several quiet years mean the issue is closed. That assumption can be costly.

The Congressional Budget Office has discussed legislation involving delinquent pandemic-related PPP and EIDL loans. That discussion reflects continued attention to collections, enforcement, and recovery. Business owners should not treat old loan obligations as harmless paperwork.

A business that received pandemic funding should know where its files are stored. It should also know whether the loan was forgiven, repaid, deferred, delinquent, or unresolved. Guessing is not a good financial control.

This is especially important for owners planning to sell, close, refinance, or reorganize a business. Unresolved debt can complicate due diligence. It can also create stress during an already sensitive transaction.

The Bottom Line for Business Owners

Pandemic loan collections remind owners that business debt does not always disappear with time. Government-backed loans may remain subject to review, collection, and enforcement long after funds are received.

For legitimate borrowers, the right response is not fear. It is careful organization and prompt action. Keep records, read notices, verify communications, and seek qualified help when needed.

For future borrowers, the broader lesson is just as important. Fast money is still borrowed money. Emergency funding can help a business survive, but documentation must survive too.

Small business owners do not need to become legal experts. They do need to treat loan records as permanent business assets. When questions arise years later, those records may become the strongest protection available.

Financial Information Disclaimer: This article is for general educational purposes only. It is not financial, legal, tax, or accounting advice. Business owners should consult qualified professionals about their specific circumstances before making financial or legal decisions.

Photo Credit: All images © Sloan Digital Publishing and licensed stock sources. Used with permission.

{kind=link}