A business dependent on financing can appear stable even while deeper financial pressure quietly builds beneath the surface. Borrowed capital can support recovery, expansion, or seasonal disruption when it is used deliberately and sparingly. Trouble begins when ordinary survival requires constant access to new credit instead of dependable operating revenue. This gradual shift weakens resilience, reduces flexibility, and increases long-term financial risk.

Many owners overlook early warning signs because daily operations continue without interruption. Employees remain paid, vendors keep shipping, and customers rarely see internal strain. Yet dependence on borrowing slowly erodes decision-making freedom and increases vulnerability to outside lenders. Recognizing these patterns early allows corrective action before markets or credit conditions force painful change.

How to Recognize a Business Dependent on Financing

Financing can be useful when it supports a clear purpose and a realistic repayment plan. Problems develop when borrowing becomes routine instead of strategic. At that point, the business is no longer using financing as a tool. Financing is beginning to function as a survival mechanism.

Cash Flow Gaps Reveal a Business Dependent on Financing

Healthy companies use financing for growth initiatives or short-term disruption. A business dependent on financing needs funding simply to maintain routine expenses each cycle. If payroll, rent, or inventory purchases depend on loan approval, structural imbalance already exists. Core operations should be sustained primarily through consistent customer revenue.

Repeated shortfalls usually indicate thin margins, rising costs, or weak collections. Financing may temporarily hide these weaknesses without correcting them. Over time, the gap between income and expenses expands further. Even a modest slowdown can then threaten stability.

These early pressures often push companies toward repeated borrowing.

Short-Term Borrowing Becomes a Permanent Cycle

Working capital loans are designed to bridge temporary needs. Constant renewal suggests the bridge has quietly become permanent infrastructure. When one loan replaces another, profitability stops driving stability. Interest costs increase while operational flexibility steadily declines.

This pattern increases vulnerability to lender policy changes or tightening credit markets. Owners may feel trapped between repayment pressure and continued borrowing. Stress rises because each month depends on outside approval. Restoring sustainable cash flow becomes the only real exit.

These warning signs often emerge when borrowing becomes a repeating cycle rather than a temporary tool. That cycle is explained in detail in our guide on why businesses become dependent on fast financing.

For deeper context, review our explanation of working capital loans and cash flow stability. Understanding intended loan use helps reveal when borrowing has crossed into dependence. That clarity supports smarter financial decisions.

Growth Funded Only by Debt Increases Risk

Expansion supported entirely through borrowing creates fragile momentum. Sustainable growth usually blends retained earnings, operational efficiency, and selective financing. When hiring, inventory, or equipment depends solely on new debt, risk may scale faster than revenue. Rapid expansion can temporarily disguise weak fundamentals.

True growth strengthens long-term cash generation and gradually reduces borrowing reliance. If debt rises faster than income, caution becomes essential. Strategic pacing often produces stronger stability than speed. Long-term endurance matters more than short-term visibility.

Financial pressure rarely stays hidden forever. Vendor relationships often reveal the strain first.

Vendor Relationships Begin Carrying Financial Strain

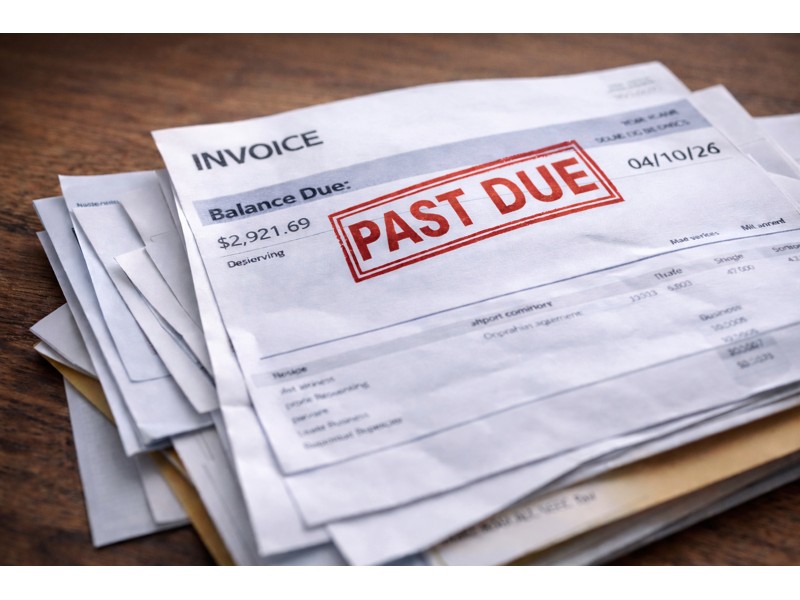

Suppliers frequently detect financial stress before lenders recognize warning signs. Slower payments, partial payments, or repeated extensions reveal tightening liquidity. Relying on vendor patience shifts financial pressure onto critical relationships. Once trust weakens, supply disruption may follow quickly.

When vendors tighten payment terms, dependence can worsen rapidly. The business may then require additional borrowing to cover faster pay cycles. This creates a compounding effect that feels sudden. In reality, the imbalance usually develops over many months.

Unexpected Costs Require Immediate New Borrowing

Equipment failure, weather damage, and urgent repairs affect every company eventually. Financial resilience depends on reserves prepared before emergencies occur. A business dependent on financing must secure borrowing before responding to routine surprises. This delay increases stress and limits available options.

Even modest emergency savings can restore decision-making control. Liquidity provides time for thoughtful planning instead of reactive borrowing. Guidance from the U.S. Small Business Administration emphasizes reserve planning as a core stability strategy. Preparation often determines survival during disruption.

Debt Service Consumes a Growing Share of Revenue

Borrowing creates repayment obligations that must remain proportional to income. When debt service grows faster than revenue, flexibility disappears quickly. Cash that could support hiring, marketing, or innovation instead services past borrowing decisions. This imbalance weakens resilience during downturns.

High repayment pressure limits recovery options when conditions soften. Owners may cut maintenance, delay marketing, or reduce staffing to compensate. Those actions often reduce revenue further. The cycle then reinforces itself.

Lenders Become the Source of Stability Instead of Customers

Financing should support stability rather than create it. When continued operations depend primarily on lender approval, dependence has already formed. External institutions begin influencing internal decisions. Credit tightening or score changes can suddenly threaten survival.

Operational stability must originate from customer demand and disciplined management. External funding should remain secondary support. Businesses regain independence by strengthening profitability and collections. Customer revenue remains the most reliable foundation.

Leadership Conversations Focus on Borrowing Rather Than Performance

Internal discussions reveal shifting priorities within an organization. Frequent focus on credit limits, refinancing, or approval timing signals deeper imbalance. Healthy companies analyze margins, efficiency, and retention trends. Dependent companies monitor borrowing capacity above operating health.

This mindset shift often develops gradually and becomes normalized. Reversing it requires disciplined financial review and clearer reporting. Leadership must reconnect decisions to sustainable profitability. Otherwise, borrowing remains the default solution.

Stress Persists Even During Revenue Growth

Revenue growth should create confidence and opportunity. Rising anxiety alongside increasing sales often signals structural weakness. Thin margins, heavy debt, or aggressive expansion can absorb new income quickly. Borrowing then fills the remaining financial gap.

This contradiction confuses many owners because performance appears positive. Hidden pressure continues intensifying beneath the surface. Without correction, growth may accelerate instability rather than reduce it. Careful analysis reveals the true condition.

Federal Reserve findings in the Small Business Credit Survey show that reliable cash flow predicts long-term stability more strongly than loan availability. Borrowing can help temporarily, but it cannot replace profitability. Sustainable revenue remains the foundation of resilience.

How to Reduce Financing Dependence and Regain Control

Recognition is the first corrective step for any business dependent on financing. Margin improvement often provides the fastest measurable relief. Small pricing adjustments, tighter purchasing controls, and improved collections can strengthen cash flow quickly. Better visibility into expenses also supports smarter planning.

Building emergency reserves restores independence from urgent borrowing. Refinancing high-cost debt into predictable structures may stabilize repayment pressure. Strategic pacing of growth prevents new financial strain. Consistent discipline gradually rebuilds resilience.

For additional guidance, review our discussion of refinancing business debt strategies. You may also find it helpful to review working capital loans and cash flow stability when evaluating whether financing still serves a strategic purpose. Clear structure supports long-term stability.

Financing Should Remain a Tool, Not a Survival Mechanism

Modern funding options remain valuable when used intentionally and strategically. Financing can enable innovation, recovery, and controlled expansion. Dependence transforms opportunity into limitation and risk. Early awareness protects both stability and lender relationships.

Financial strength ultimately comes from customers, value creation, and disciplined management. Borrowing should support that foundation rather than replace it. Businesses that restore balance regain flexibility and confidence. Sustainable cash flow determines long-term resilience.

Financial Disclaimer: This article provides general educational information only and does not constitute financial, legal, or tax advice. Consult qualified professionals for guidance specific to your business situation.

Photo Credit: All images © Sloan Digital Publishing and licensed stock sources. Used with permission.

{kind=link}