Fast funding can look like a smart answer during a difficult cash flow stretch. Yet short-term business loan risks often appear after the money arrives, not before. Many owners focus on approval speed first, then discover that repayment pressure creates a second and more serious problem.

That pattern is common because short-term lending is designed to solve urgency. The pitch is often simple, fast, and emotionally persuasive. The structure behind the offer, however, may drain working capital faster than expected and weaken the business at the wrong time. These short-term business loan risks often remain hidden until repayment begins.

Experienced owners usually understand that debt carries cost. What they sometimes underestimate is the effect of repayment timing on daily operations. A loan that looks manageable on paper can still damage payroll flexibility, vendor timing, and purchasing decisions.

Why short-term financing attracts capable business owners

Most borrowers do not seek short-term funding because they are careless. They seek it because pressure compresses decision time. A tax bill, inventory need, equipment failure, seasonal gap, or delayed receivable can make fast money feel responsible.

Lenders understand that emotional reality very well. Their marketing often emphasizes convenience, speed, and relief. Those features matter, but they do not tell the full story of the obligation being created.

A short-term loan can be useful in a narrow set of cases. It may help bridge a clearly defined gap with a visible repayment source. Problems begin when the financing is used to cover recurring weakness rather than a short-lived disruption.

Why short-term business loan risks are driven by structure

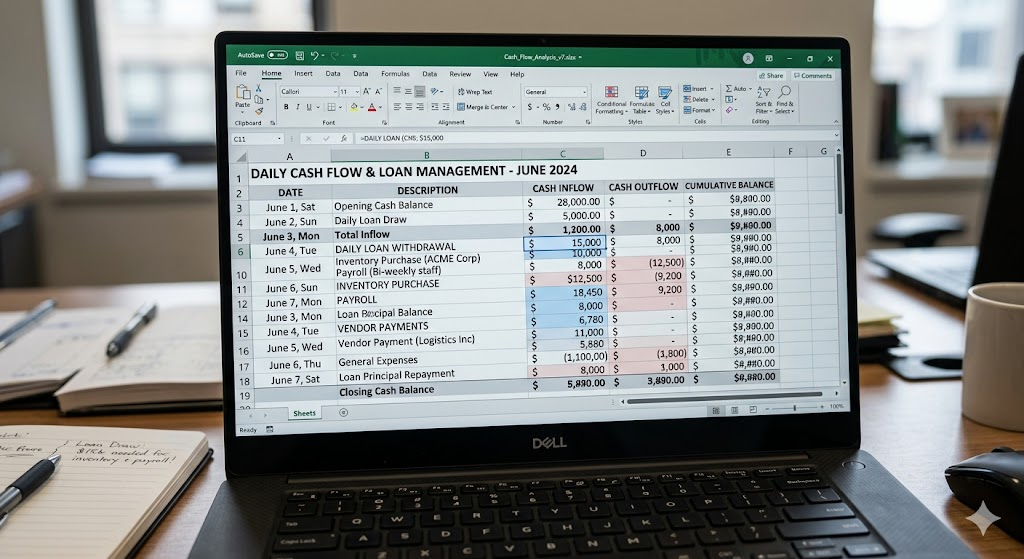

The real issue is not simply interest. Structure usually determines whether the loan supports the business or strains it. Daily or weekly withdrawals, fixed payment schedules, and compressed maturities can change the economics quickly.

Some owners focus on whether they can qualify. A better question is whether the business can absorb repayment without harming operations. That answer depends on margin strength, cash timing, and how much room already exists in the system.

Even a profitable company can struggle with a poorly timed repayment schedule. Cash flow does not move in a straight line every week. When debt assumes steadier inflows than the business actually generates, stress grows rapidly.

Repayment frequency changes the pressure level

Monthly payments are easier to evaluate because they align with most budgeting habits. Daily or weekly withdrawals feel smaller, but they often create more operational friction. They reduce flexibility before the owner has time to adjust.

That matters because businesses pay for surprises with liquid cash. When withdrawals hit too often, management loses room to respond. Small setbacks then become larger decisions involving delayed purchases, late payments, or reduced staffing hours.

In practical terms, repayment frequency can matter as much as the rate itself. A higher-cost loan with manageable timing may be less disruptive than a lower-cost product with relentless withdrawals. Owners should judge both issues together.

Total borrowing cost is not always obvious at first glance

Short-term products are often presented in ways that feel easier to digest. Owners may see a factor rate, a flat fee, or a simple repayment number. Those figures can hide the real annualized cost and reduce comparison quality.

That does not mean every product is deceptive. It does mean that cost disclosure can be less intuitive than a traditional term loan. Before signing, owners should translate the structure into total dollars paid and the practical burden on cash flow.

The Federal Trade Commission advises business owners to review terms carefully and understand total repayment obligations before accepting financing. That is basic guidance, but it remains highly relevant when speed is involved. Federal Trade Commission business guidance

How short-term business loan risks spread through daily operations

Many lending decisions are judged too narrowly at the moment of funding. Owners often ask whether the money solves the immediate problem. A stronger analysis asks what that repayment schedule will do over the next ninety days.

Once withdrawals begin, pressure moves through the business in layers. Cash reserved for inventory may shrink. Vendor timing may tighten, payroll decisions may become harder, and marketing may be cut at the exact moment growth is needed.

These effects rarely appear as one dramatic collapse. They usually show up as a series of smaller compromises. Each compromise seems manageable alone, but together they weaken resilience and decision quality.

A company that was already tight on receivables is especially vulnerable. If customer payments arrive late while loan withdrawals continue on schedule, the business may borrow against uncertainty. That is a dangerous position for any owner.

This is one reason accounts receivable management matters so much before new debt is added. If collections are weak, financing can temporarily mask the problem instead of solving it. Owners should fix internal cash flow leaks before layering on new obligations. Read our guide to accounts receivable mistakes that hurt cash flow

Cash flow pressure rarely exists in isolation. It often connects to broader liquidity issues that develop over time. Owners who understand how financing dependence builds can avoid repeating the same cycle under increasing pressure. Explore how financing dependence quietly reshapes business decisions over time

When short-term business loan risks signal a deeper problem

Not every cash shortage is temporary. That distinction matters more than many lenders will admit. A bridge loan can help with timing, but it cannot repair weak margins, chronic overspending, or a broken pricing model.

Owners should pause when funding is needed to cover ordinary operating costs month after month. That pattern suggests a structural issue inside the business. In those cases, fast capital often delays a correction that should happen sooner.

Another warning sign appears when projected repayment depends on optimistic assumptions. If sales must improve quickly for the loan to remain comfortable, risk has already increased. Sound borrowing should not require best-case performance just to stay current.

The same concern applies when debt is used to replace discipline. If inventory purchasing lacks control, expense growth is unchecked, or customer concentration is too high, borrowing may deepen exposure. Money should support a plan, not substitute for one.

Signs dependency may be forming

Dependency usually begins quietly. One loan closes a gap, then another addresses the pressure created by the first repayment cycle. The business becomes more focused on access to money than on restoring financial balance. This is where short-term business loan risks begin compounding instead of resolving.

That cycle can be difficult to detect because activity remains high. Revenue may still be coming in, staff may remain busy, and customers may see no visible distress. Internally, however, management time becomes dominated by cash timing rather than strategy.

When financing starts to fund prior financing, the warning is serious. At that stage, debt may be sustaining appearance rather than strength. Owners should step back and examine whether the business still has healthy operating economics.

Questions to ask before signing any short-term loan

First, identify the exact problem the loan will solve. Vague purposes usually produce weak borrowing decisions. A precise need creates a better standard for judging whether the structure fits.

Second, map repayment against actual cash inflows, not hopeful forecasts. Use conservative assumptions and include uneven weeks. If the schedule still works under stress, the loan deserves further consideration.

Third, calculate total cost in dollars and compare it with the expected benefit. Speed has value, but it is not free. Owners should know what relief truly costs before accepting convenience as a business strategy.

Fourth, ask what happens if receivables slow, a major customer delays payment, or sales dip for thirty days. If the business has no safe answer, the financing may be too aggressive. Stress testing should happen before commitment, not after.

The U.S. Small Business Administration encourages owners to understand financing terms, compare options, and align borrowing with business needs. That advice may sound simple, but discipline often collapses under time pressure. U.S. Small Business Administration loan guidance

Safer alternatives before accepting fast money

Sometimes the best financing decision is not a loan at all. Receivables follow-up, inventory reduction, payment term renegotiation, and disciplined expense cuts can release cash without creating new obligations. Those actions are rarely exciting, but they are often effective.

Owners should also evaluate whether a line of credit fits better than a compressed short-term product. A well-structured revolving option can offer flexibility with less constant repayment pressure. Qualification may be harder, but the long-term outcome may be healthier.

In some cases, staged borrowing is wiser than taking the full requested amount. Smaller financing can reduce risk while preserving options. It also forces sharper thinking about what problem truly needs to be funded.

Another overlooked option is delaying expansion until internal systems improve. That may feel frustrating, but restraint can protect future capacity. Borrowing works best when it strengthens momentum that already exists, not when it tries to create stability from weakness.

Good financing should create room, not remove it

Short-term lending is not automatically bad. In the right situation, it can solve a narrow and temporary problem with reasonable efficiency. The danger begins when owners judge the product by approval speed instead of operational impact.

Healthy borrowing should give a business room to function, adapt, and grow. It should not quietly drain flexibility every week while management becomes more reactive. Owners who examine timing, total cost, and dependency risk make better decisions than those who focus on access alone.

That is the real lesson behind short-term business loan risks. Fast money should support a business that already has a workable plan. When the loan becomes the plan itself, the risk is no longer temporary. Recognizing short-term business loan risks early is what separates stable companies from reactive ones.

Financial Information Disclaimer

This article is provided for general educational purposes only. It does not constitute financial, legal, tax, or lending advice. Business owners should review financing decisions with qualified financial, legal, and tax professionals before acting.

Photo Credit:

All images © Sloan Digital Publishing and licensed stock sources. Used with permission.

{kind=link}