Editor’s Note: This Business Loan Press article has been updated for clarity, readability, and current small business financing standards.

Financing can help a business grow, stabilize cash flow, buy equipment, expand inventory, or manage a temporary gap between expenses and revenue. However, business loan approval is not based on need alone. Lenders want to see organized records, repayment ability, clear loan purpose, and a borrower who understands the terms being offered.

Many owners hurt their chances before the lender has fully reviewed the file. Some submit incomplete documents, request the wrong amount, ignore credit problems, or choose a lender that does not fit their situation. Avoiding common business loan application mistakes can improve approval odds and help owners avoid poor loan terms.

A stronger application does not guarantee approval, but it can make the process smoother. It can also help a lender understand the business more quickly and evaluate the request with fewer delays. Before applying, review the mistakes below and correct as many as possible.

Submitting Incomplete or Disorganized Documentation

One of the most common business loan application mistakes is submitting documents that are missing, outdated, or difficult to follow. Underwriters make decisions from records, not intentions. If they cannot quickly verify revenue, expenses, debt, ownership, and cash flow, the application may slow down or lose credibility.

Most lenders want to see recent business bank statements, tax returns, financial statements, debt schedules, and basic legal documents. Depending on the loan type, they may also request leases, contracts, licenses, insurance information, or accounts receivable reports. A clean, organized file reduces back-and-forth and makes the borrower look more prepared.

Before applying, create a folder with clearly labeled documents. Make sure the numbers are consistent across tax returns, profit and loss statements, balance sheets, and bank deposits. If something looks unusual, prepare a short explanation before the lender asks.

Applying Without a Clear Loan Purpose

A lender will want to know why the money is needed and how it will be used. A vague request such as “business expenses” or “growth” may not be enough. The purpose should be specific, measurable, and connected to the business’s ability to repay.

For example, a request to buy inventory before a seasonal sales period is easier to evaluate than a general request for extra cash. A request to purchase equipment should include the cost, expected use, and how the equipment may improve revenue or efficiency. A request for working capital should explain the timing gap the loan is meant to cover.

A clear use-of-funds statement helps the lender understand the need and assess whether the loan type fits the purpose. It also helps the owner stay disciplined after funding. Borrowed money should have a defined job inside the business.

Skipping the Business Plan or Weakening the Story

Not every loan requires a long formal business plan, but every application should tell a coherent business story. The lender should understand what the business does, how it earns money, who its customers are, and why the loan makes financial sense. A weak or missing plan can make even a promising business look unprepared.

The plan should connect the loan request to realistic outcomes. Include market context, revenue sources, operating milestones, and repayment logic. Projections should be based on reasonable assumptions, not best-case hopes.

If your business has faced challenges, do not ignore them. Explain what happened, what changed, and how the business is positioned now. Lenders value clarity, especially when the owner can show that problems have been identified and addressed.

Not Understanding Loan Requirements Before Applying

Different loan programs have different requirements. Some lenders emphasize credit scores and time in business. Others focus more heavily on revenue, cash flow, collateral, industry risk, or existing debt.

Applying blindly can waste time and create unnecessary frustration. A borrower who does not meet the basic requirements may receive a quick denial even if the business is otherwise healthy. That is why owners should review eligibility guidelines before submitting an application.

For a broader preparation guide, review Business Loan Press’s article on items banks may require before approving a business loan. Understanding lender expectations before applying can prevent avoidable delays.

Ignoring Personal and Business Credit

Credit health can affect both approval and pricing. Many small business owners focus only on business credit and forget that personal credit may also be reviewed, especially for smaller businesses or newer companies. This is one of the business loan application mistakes that can surprise borrowers late in the process.

Before applying, check both personal and business credit reports when possible. Look for errors, late payments, high utilization, unresolved collections, or accounts that need explanation. Even modest improvements may help the application look stronger.

Paying bills on time, reducing revolving balances, and avoiding unnecessary new debt can help strengthen the file. If credit issues remain, be prepared to explain them honestly. A lender may respond better to a clear explanation than to a problem that appears hidden.

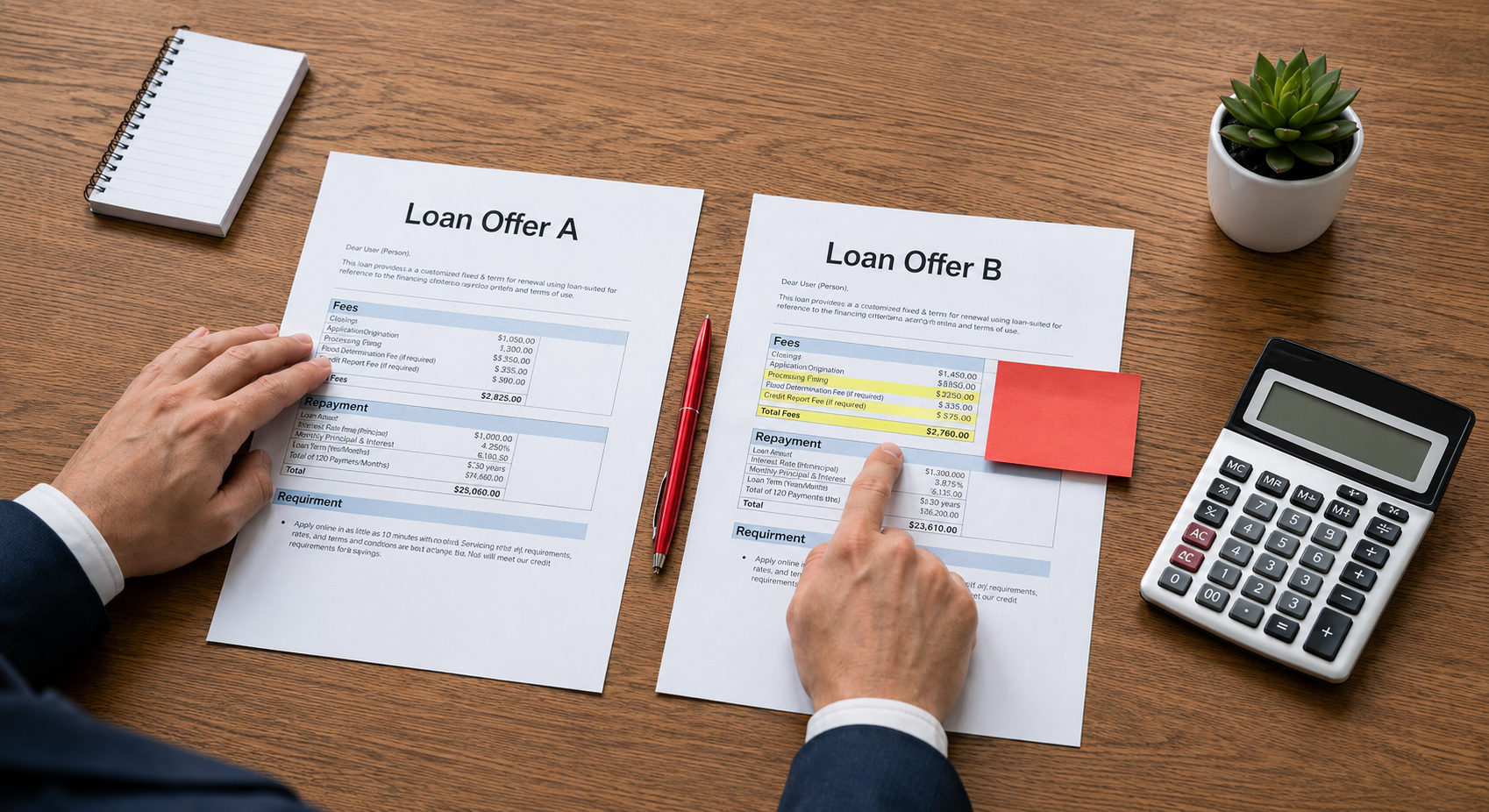

Requesting the Wrong Loan Amount

Requesting too little can leave the business underfunded. Requesting too much can make the lender question the owner’s planning and repayment ability. The amount should be built from actual costs, not guesswork.

Start with the intended use of funds. Price equipment, inventory, marketing, payroll, buildout, or operating needs as accurately as possible. Then include a reasonable cushion for related expenses without inflating the request beyond what the business can repay.

Use repayment estimates to test affordability before applying. Business owners can also review Business Loan Press’s guide on using a business loan calculator to plan repayment. The right loan amount should support the business without creating avoidable cash flow strain.

Hiding or Downplaying Business Risks

Optimism is useful in business, but lenders expect honesty. If a borrower hides risks, avoids obvious weaknesses, or provides overly rosy projections, the lender may lose confidence in the file. Transparency can be more persuasive than pretending everything is perfect.

Common risks include customer concentration, seasonal revenue, rising costs, supply chain issues, industry pressure, thin margins, or recent sales declines. These risks do not always prevent approval. However, they should be acknowledged and addressed.

Explain how the business manages risk. You might point to insurance, diverse suppliers, long-term contracts, cash reserves, cost controls, or a broader customer base. A lender wants to know that the owner recognizes potential problems and has a plan to respond.

Choosing the Wrong Lender

Not every lender is a good fit for every business. Banks, credit unions, community lenders, SBA-approved lenders, online lenders, and specialty finance companies may evaluate applications differently. Choosing the wrong lender can waste time and lead to poor terms.

A traditional bank may offer competitive pricing but require stronger documentation and a longer review. Online lenders may move faster but charge more or require more frequent payments. Community banks and credit unions may offer relationship-based service, while nonprofit lenders may provide smaller loans with added support.

Compare several options before applying. Look at total repayment cost, fees, repayment schedule, collateral, personal guarantee language, lender reputation, and reporting practices. The best lender is not always the one that advertises the fastest funding.

Overlooking Collateral and Personal Guarantees

Collateral and guarantees can affect both business and personal risk. Some loans require specific assets, such as equipment, inventory, receivables, vehicles, or real estate. Others may require a blanket lien or a personal guarantee from the owner.

A personal guarantee may make the owner personally responsible if the business cannot repay. This can expose personal credit or assets depending on the agreement. Owners should never assume that a business loan affects only the business.

Before signing, ask what assets are at risk, whether the lien is blanket or asset-specific, and when any lien may be released. For more background, read The Role of Collateral in Small Business Loans. Understanding collateral and guarantee language is essential before accepting funding.

Lacking a Clear Repayment Strategy

Approval depends heavily on repayment confidence. A lender wants to see that the business can make payments from normal operations, not from hope or emergency borrowing. A repayment strategy should be specific and realistic.

Show how the payment fits within the business’s cash flow. Include conservative assumptions and consider slow periods, delayed receivables, or seasonal dips. If repayment only works under perfect conditions, the loan may be too risky.

It also helps to identify early warning signs. If sales fall below a certain level or expenses rise unexpectedly, the owner should know what adjustments may be needed. A repayment plan is stronger when it includes both expected performance and backup thinking.

Ignoring Fees, Covenants, and Hidden Clauses

A low advertised rate does not always mean a low-cost loan. Origination fees, documentation fees, late fees, servicing fees, prepayment penalties, and required insurance can change the true cost. Borrowers should compare the total repayment amount, not just the monthly payment.

Loan covenants and restrictions also matter. Some agreements may require financial reporting, limit additional borrowing, restrict asset sales, or require certain financial ratios. These terms can affect business flexibility long after the loan is approved.

Ask for a full fee list and review the agreement carefully. Confirm whether the rate is fixed or variable, whether prepayment is allowed, and what happens if the business misses a covenant or payment. These details can determine whether the loan remains manageable.

Applying at the Wrong Time

Timing can influence how the business looks on paper. Applying during a revenue dip, before books are reconciled, or before tax filings are complete can weaken the application. Lenders often evaluate recent performance, so messy timing can create unnecessary problems.

When possible, apply after strong operating months and with clean records. Make sure bank statements, financial reports, and tax returns are consistent. Avoid major unexplained changes in deposits, expenses, or debt right before applying.

Owners should also avoid waiting until the business is desperate. A rushed application can lead to limited options and expensive terms. Planning early gives the business more time to compare lenders and prepare a stronger file.

Underestimating Digital Underwriting

Many lenders now rely on digital tools, bank-data connections, automated scoring, and standardized reporting. That does not mean human judgment has disappeared, but it does mean inconsistent data can create problems quickly. Clean records matter more than ever.

Bank deposits, merchant processing records, accounting reports, and tax documents should tell a consistent story. If the numbers do not align, the lender may request explanations or decline the file. Owners should review digital records before giving a lender access or submitting documents.

Digital underwriting rewards organization. Accurate bookkeeping, separated business accounts, steady deposits, and clean reports can make the process easier. Messy records can make a healthy business look riskier than it is.

Skipping Professional Guidance

Some business owners try to handle the entire loan process alone. That may work for a simple application, but professional guidance can be valuable when the loan amount is large, the business is complex, or the terms are unfamiliar. An accountant, attorney, bookkeeper, or business advisor may spot weaknesses before the lender does.

An accountant can review projections, cash flow, tax consistency, and debt coverage. An attorney can help evaluate contract language, collateral, guarantees, and default clauses. A business mentor may help clarify the plan and prepare better explanations.

Professional guidance does not remove the owner’s responsibility. It helps the owner make a more informed decision. A cleaner file and better understanding can prevent avoidable mistakes.

Documentation Checklist for a Smoother Review

A complete application package can reduce delays and improve credibility. The exact list will vary by lender and loan type, but many applications require similar core documents. Preparing these items early can save time.

- Business tax returns

- Personal tax returns, if required

- Recent business bank statements

- Profit and loss statement

- Balance sheet

- Cash flow forecast

- Debt schedule

- Business plan or use-of-funds summary

- Legal formation documents

- Leases, contracts, licenses, or insurance documents when relevant

Keep the file organized and consistent. If the lender asks for additional documents, respond promptly and clearly. A professional, complete file can make the borrower easier to underwrite.

Why Avoiding These Mistakes Matters

A business loan application is more than a request for money. It is a presentation of the business’s financial health, management discipline, and repayment ability. Errors can create doubt even when the business itself is strong.

Avoiding business loan application mistakes can save time, reduce frustration, and improve the chance of receiving better terms. Clean data, conservative projections, and clear explanations make the lender’s job easier. They also help the owner borrow with more confidence.

The goal is not merely to get approved. The goal is to secure financing that fits the business and supports long-term stability. A bad loan can be more damaging than no loan at all.

Final Thoughts

Avoiding business loan application mistakes takes preparation, discipline, and honesty. Organize documents, review credit, right-size the request, compare lenders, and understand the agreement before signing. These steps can protect both approval odds and future cash flow.

Business financing should support the company, not create new problems. When owners apply with clean records, realistic numbers, and a clear repayment plan, they give lenders more reason to trust the request. They also give themselves a better chance of choosing a loan that truly fits.

Sources

- U.S. Small Business Administration: Loan Programs

- U.S. Small Business Administration: Fund Your Business

- SCORE: Requirements for a Small Business Loan

- Consumer Financial Protection Bureau: Small Business Lending

- Investopedia: Small Business Loan Mistakes

This article is for general educational purposes only and should not be considered legal, financial, or lending advice. Business owners should review loan agreements carefully and consult a qualified professional when needed.

Photo Credit: All images © Sloan Digital Publishing and licensed stock sources. Used with permission.

{kind=link}