PPP and EIDL records can become important long after a business owner expects to need them. A notice, lender question, audit request, collection issue, or future loan application can suddenly make old pandemic files relevant again. Recent SBA collection activity is a reminder that pandemic-era business financing did not simply disappear with time. Good documentation can help owners answer questions, correct errors, and protect their financial position.

Many business owners placed those files away once forgiveness, repayment, or closure issues seemed settled. That reaction is understandable. Pandemic loan programs moved quickly because businesses needed help fast. That speed helped many companies survive an extraordinary period.

It also created confusion about eligibility, forgiveness, repayment, and long-term recordkeeping. Some owners kept excellent files, while others relied on scattered emails or memory. Business owners do not need to panic over old loan files. They do need to know where those files are and what they contain.

Why PPP and EIDL Records Still Deserve Attention

The Paycheck Protection Program and COVID Economic Injury Disaster Loan program were not ordinary business financing products. They were emergency programs created during a national crisis. Because of that, they included special rules, changing guidance, and detailed eligibility requirements.

PPP loans often involved payroll calculations, forgiveness applications, employee counts, and permitted use categories. COVID EIDL loans focused more on working capital needs and repayment obligations. Both programs created documentation trails that owners may still need.

The Small Business Administration remains the central agency for many pandemic loan issues. Treasury collection activity and enforcement attention have also kept older files relevant. That does not mean every borrower faces a problem. It means business owners should not treat those records as disposable.

A missing document can make a simple question harder to answer. A complete file can help show what happened, when it happened, and why. That clarity is valuable during audits, disputes, repayment reviews, and future loan applications.

PPP and EIDL Records Can Separate Errors From Serious Concerns

Not every loan problem involves fraud. Businesses can run into repayment trouble for many honest reasons. Revenue may have dropped, ownership may have changed, or communication may have been missed. Some owners may also have misunderstood program rules during a stressful period.

Fraud concerns are different. They may involve false statements, fake businesses, inflated payroll, identity theft, or misuse of funds. Those allegations can carry serious civil or criminal consequences. Documentation helps create an important distinction.

Clear records can show that an owner applied in good faith. They can also show how funds were received and used. If an error occurred, records may help identify whether it was clerical, financial, or legal. That difference can affect the next step.

Owners should avoid casual explanations when serious questions arise. A quick phone conversation may not be enough. Written records, professional advice, and careful review are usually safer.

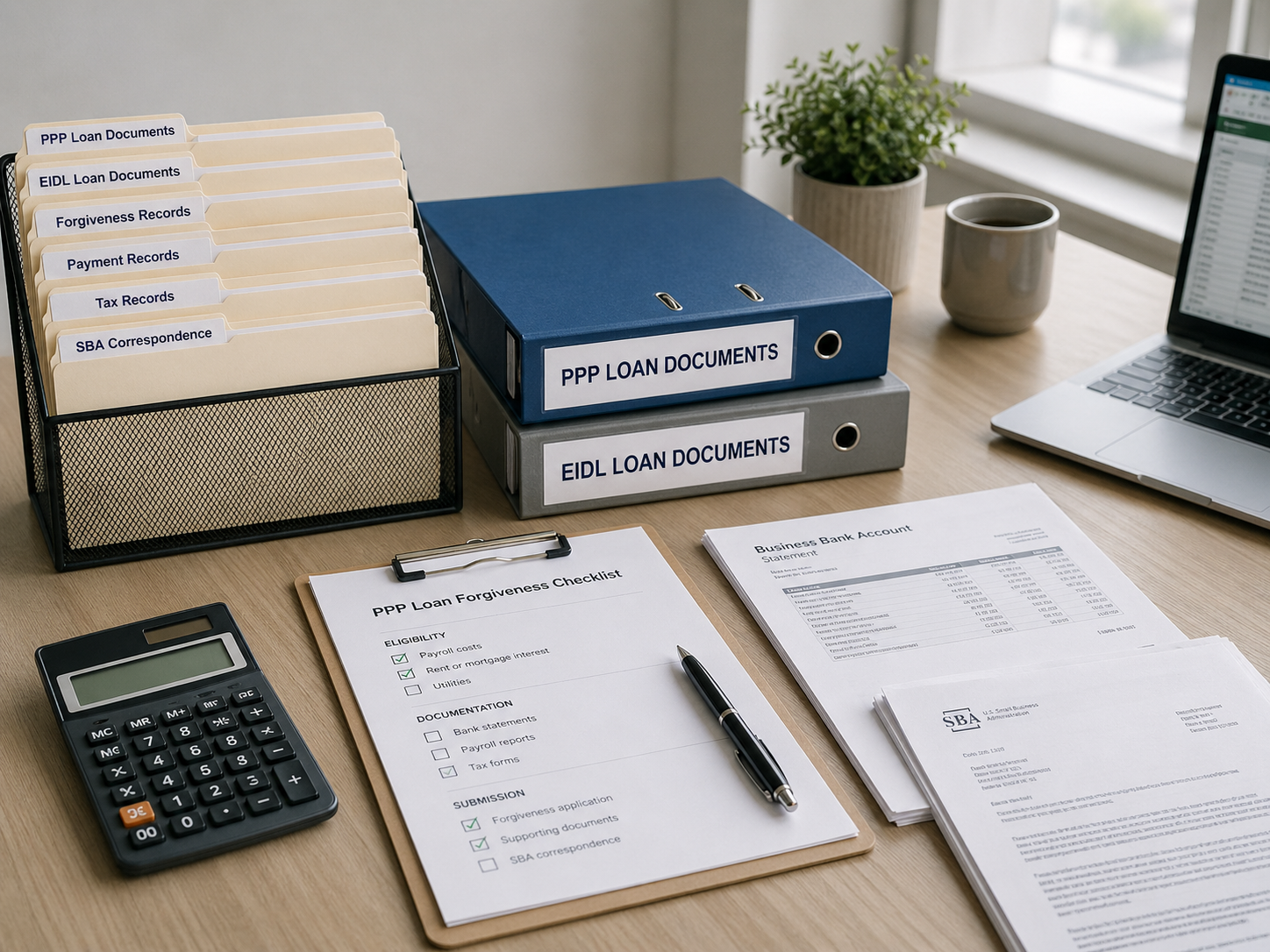

What Business Owners Should Keep in Their Loan Files

A strong PPP and EIDL records file should begin with the original application. Include the loan number, approval notice, promissory note, and lender correspondence. Keep any SBA messages, account portal screenshots, and payment confirmations.

For PPP loans, include payroll reports used for the application. Keep tax forms, employee rosters, wage records, and benefit cost documentation. Owners should also keep forgiveness applications and approval notices. If forgiveness was denied or reduced, keep that correspondence too.

For EIDL loans, keep the loan agreement and repayment schedule. Include bank records showing receipt of funds and later payments. If the loan was deferred, modified, or placed into hardship status, keep those notices.

At minimum, a business owner should try to keep five core items together. These include the loan application, approval documents, forgiveness or repayment records, bank statements, and proof of fund use. Those records create a basic timeline that can help explain the loan from application through resolution.

Owners should also save proof of how funds were used. Useful records may include payroll summaries, rent payments, utility bills, vendor invoices, insurance costs, and bank statements. These documents help connect loan proceeds to business activity.

For broader guidance, business owners may also review business loan documentation before applying for future financing. Good habits often carry from one loan file to the next.

Why Organized PPP and EIDL Records Help Future Borrowing

Old loan files can affect more than past obligations. Future lenders may ask about prior SBA loans, business debt, or repayment history. A disorganized file can slow the process. It can also create doubts that might have been avoided.

Strong records help owners answer lender questions with confidence. They also support cleaner financial statements and stronger loan applications. That is important when applying for term loans, lines of credit, equipment financing, or refinancing.

Business financing often depends on trust. Lenders want to see that owners understand their obligations. Organized records suggest financial discipline. They can also reduce delays during underwriting.

This is especially important for newer business owners. The same habits used to manage PPP and EIDL records can support future borrowing. Clean files make it easier to document revenue, expenses, tax history, and repayment ability.

Owners preparing for new financing can also read more about applying for a small business loan. A complete documentation process can reduce stress before an application begins.

PPP and EIDL Records May Help During Collections

If a collection notice arrives, business owners should not ignore it. The first step is to confirm that the notice is real. Scams can follow government collection headlines, especially when borrowers feel anxious.

Owners should compare the notice with their own records. Review the loan number, balance, payment history, forgiveness status, and agency contact details. If something appears wrong, document the issue before responding.

Good records can help support a dispute, correction request, or repayment conversation. They may also help an adviser understand the situation quickly. Without records, even a valid concern can become harder to explain.

Business owners should keep notes from every call. Record dates, names, reference numbers, and instructions. Follow up in writing whenever possible. Clear communication can prevent confusion from growing.

For related guidance, owners may also review pandemic loan collections. That topic is closely connected to loan records, repayment notices, and Treasury referrals.

How Long Should Business Owners Keep Pandemic Loan Records?

Record retention rules can vary by document type and business situation. Tax records, payroll records, loan agreements, and forgiveness documents may each have different practical uses. Because of that, owners should avoid destroying pandemic loan records too quickly.

A cautious approach is usually best. Keep core loan records, forgiveness approvals, repayment records, and fund-use documentation for several years. Some owners may decide to keep digital copies permanently.

Storage does not need to be complicated. Create one folder for PPP records and one folder for EIDL records. Use clear file names with dates, document types, and loan numbers when appropriate.

Digital backups are helpful, but they should be secure. Store files in more than one safe location. Protect sensitive documents that include Social Security numbers, tax IDs, bank details, or payroll data.

Owners should also tell trusted advisers where key records are located. A CPA, bookkeeper, or attorney may need access during a review. Clear organization saves time when a deadline is approaching.

When to Get Professional Guidance

Some questions can be handled with careful record review. Others require professional help. Business owners should recognize the difference early.

A CPA may help review payroll, tax, and bank records. A bookkeeper may help organize older files. An attorney may be needed if fraud, identity theft, personal liability, or collection action appears possible.

Owners should not wait until a deadline has passed. Early guidance can preserve options and reduce mistakes. It can also prevent emotional decisions during a stressful notice or investigation.

Professional help is especially important if records do not match agency information. It is also important when ownership has changed, the business has closed, or the loan involved complex forgiveness issues. Those situations can require careful handling.

The Bottom Line on PPP and EIDL Records

PPP and EIDL records are more than old pandemic paperwork. They are part of a business’s financial history. They may help answer questions about eligibility, fund use, forgiveness, repayment, and later collection activity.

For honest borrowers, good records provide protection and clarity. They can help explain decisions made during a difficult period. They can also support future financing and stronger business controls.

Business owners should not wait for a notice before organizing these files. A careful review now may prevent confusion later. It may also uncover missing documents while they are still easier to find.

The practical lesson is simple. Borrowed money creates records, and those records should outlast the loan. For PPP and EIDL borrowers, organized files may still be one of the strongest safeguards available.

Strong recordkeeping is not just defensive. It is part of responsible business ownership. Owners who can document past financing clearly are usually better prepared for future borrowing, lender review, and long-term financial decisions.

Financial Information Disclaimer: This article is for general educational purposes only. It is not financial, legal, tax, or accounting advice. Business owners should consult qualified professionals about their specific circumstances before making financial or legal decisions.

Photo Credit: All images © Sloan Digital Publishing and licensed stock sources. Used with permission.

{kind=link}