Business credit for new business owners can feel confusing at first. Many owners hear the term before they understand what it means. They may also wonder whether business credit is separate from personal credit. The answer is yes, but the two can still overlap.

Business credit is part of a company’s financial reputation. It can affect vendor terms, credit card terms, loan options, insurance reviews, and lenders’ confidence. For newer owners, it usually takes time to build. That makes early habits especially important.

A strong business credit profile does not appear overnight. It grows from consistent records, separate accounts, timely payments, and careful borrowing. New owners do not need to chase credit quickly. They need to build it responsibly.

For many new owners, the confusing part is knowing which steps matter first. The best starting point is not a perfect credit profile. It is a business that keeps clean records, pays carefully, and separates company finances from personal spending.

Why Business Credit for New Business Owners Matters

Business credit helps lenders, vendors, and other companies evaluate financial reliability. It can show whether a business pays bills on time. It may also show how much credit the business uses and how long accounts have been open.

For a new business, the credit profile may be thin or nonexistent. That is normal. A company usually needs time, accounts, and payment history before business credit becomes meaningful.

Even so, early decisions can shape future financing. A missed payment, disorganized account, or careless credit choice can create problems later. Strong habits can help a young business look more credible over time.

Business credit should be viewed as a long-term asset. It may not solve every funding challenge. However, it can support better options when the business becomes ready to borrow.

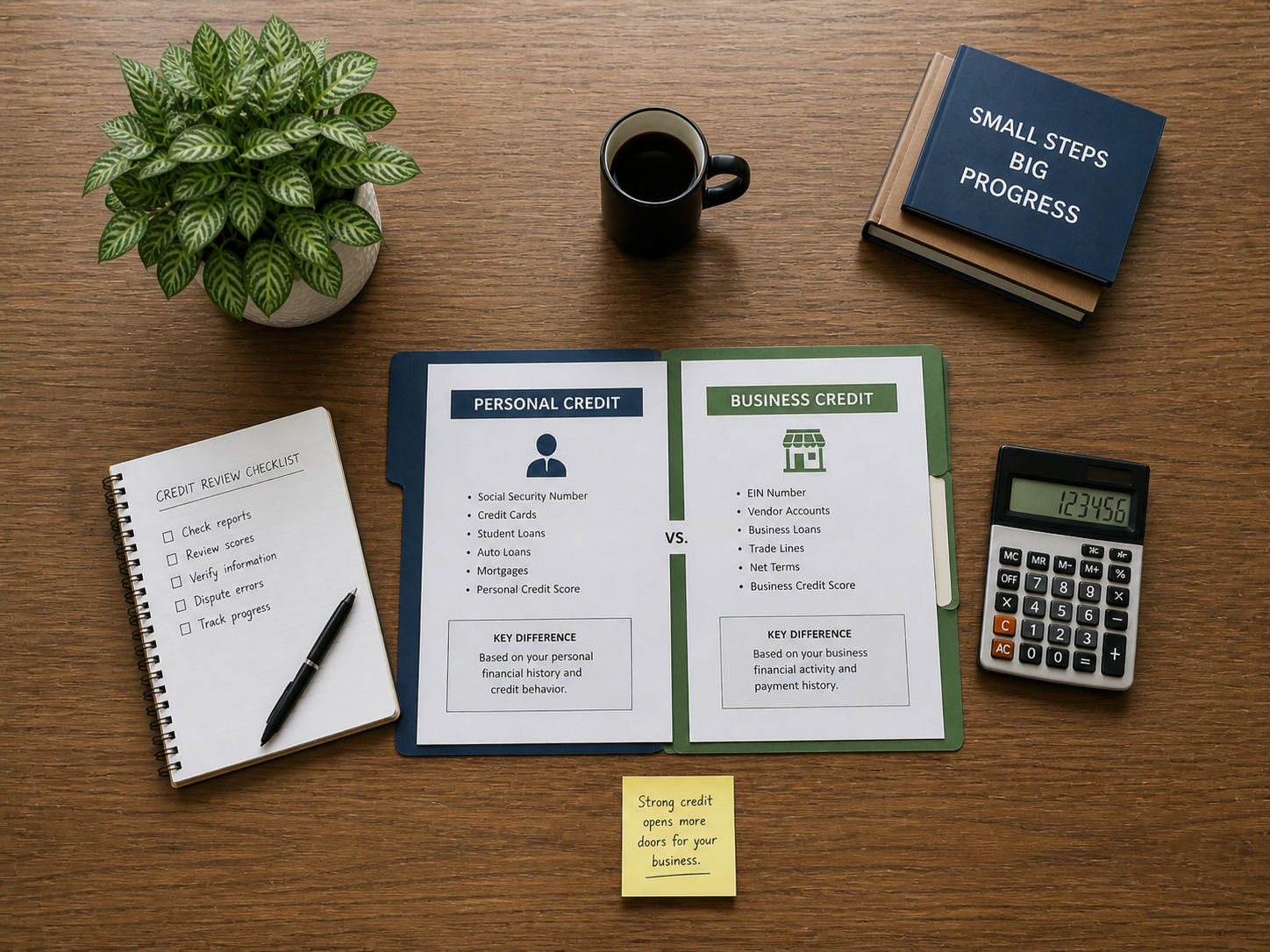

Business Credit Is Not the Same as Personal Credit

Personal credit belongs to an individual. It is tied to personal loans, credit cards, mortgages, payment history, and other consumer accounts. Business credit belongs to the company and reflects business-related financial behavior.

That difference is important. A business owner may have excellent personal credit while the company has no business credit history yet. Another owner may have business accounts but weak personal credit that still affects financing.

Newer businesses often depend on the owner’s personal credit during the early stages. Lenders may review personal credit because the business has little history. Some lenders may also require a personal guarantee.

This does not mean personal and business finances should stay mixed. In fact, separating them is one of the first steps toward stronger business credit. Clear separation helps both recordkeeping and lender review.

Start With Separate Business Finances

A business checking account is one of the simplest foundations for credit readiness. It helps separate company income and expenses from household finances. That separation makes records cleaner and decisions easier.

New owners should avoid using one account for everything. Mixed spending can make financial statements harder to understand. It can also create tax, accounting, and loan application problems.

Separate accounts help show that the business operates as a real financial entity. They also make it easier to track revenue, expenses, deposits, and withdrawals. Lenders usually prefer clean records over reconstructed explanations.

For many owners, this step should come before applying for financing. It supports better cash flow review and stronger documentation. It also helps create habits that business credit depends on.

For related preparation, business owners may also review how to prepare before applying for your first small business loan. Loan readiness often begins before an application is submitted.

How Business Credit Starts to Develop

Business credit can begin developing when a company opens accounts in its own name. These accounts may include vendor terms, business credit cards, equipment financing, or other business obligations. The Small Business Administration also recommends managing business finances with clear records and planning. Not every account reports to business credit bureaus.

That last point is important. A vendor may extend payment terms without reporting activity. Another vendor may report payment history to business credit agencies. Owners should ask how accounts are handled before assuming they help.

Timely payment is one of the most important habits. Paying late can damage trust and reduce future options. Paying early or on time may support a stronger business reputation.

Credit history also takes time. A new account is only the beginning. The real value comes from months and years of responsible use.

Why Personal Credit May Still Affect Business Financing

Many new owners are surprised when lenders ask about personal credit. This is common for young businesses. If the company lacks history, the owner’s credit may help the lender evaluate risk.

Personal credit can affect approval, loan amount, interest rate, and required guarantees. It may also influence whether the lender asks for collateral. A strong business idea may still need strong financial support.

Owners should review personal credit before seeking business financing. Errors, high balances, or recent late payments can weaken an application. Correcting problems early may improve the overall loan picture.

That does not mean a lower personal credit score makes financing impossible. It may mean options are narrower, more expensive, or require more documentation. Knowing that before applying can prevent frustration.

Use Vendor Accounts Carefully

Vendor credit can help a business manage ordinary purchases. A supplier may allow payment in 15, 30, or 60 days. This can support cash flow when used responsibly.

New owners should not open vendor accounts just to create credit activity. The account should serve a real business purpose. Buying unnecessary supplies to build credit is rarely wise.

When choosing vendors, ask whether payment activity is reported. Also ask about payment terms, late fees, order minimums, and account requirements. Understand the agreement before relying on it.

Vendor accounts work best when they support normal operations. They can become a quiet part of a company’s credit history. They should not become a substitute for careful cash management.

Understand Business Credit Cards Before Using Them

Business credit cards can be useful tools, but they can also create risk. They may help separate expenses, track purchases, and manage short-term needs. However, balances can grow quickly when owners are under pressure.

Before opening a card, review the interest rate, fees, rewards, limits, and repayment rules. Rewards should never be the main reason to carry debt. Interest charges can erase any benefit quickly.

Owners should also know whether the card activity reports to business credit bureaus, personal credit bureaus, or both. Some business cards may still affect personal credit. That detail matters before applying.

A business credit card should support disciplined spending. It should not become a way to avoid looking at cash flow. Paying the balance on time is more important than chasing a higher limit.

Business Credit and Cash Flow Work Together

Business credit is not just about opening accounts. It is closely connected to cash flow. A business with weak cash flow may struggle to make timely payments, even with access to credit.

New owners should understand monthly income and expenses before taking on credit obligations. A payment that looks small at first can become stressful during slower months. Seasonal businesses should be especially careful.

Strong cash flow can help a business use credit wisely. It gives owners more control over repayment. It can also reduce dependence on high-cost borrowing during emergencies.

For a deeper look at this issue, owners may later review why cash flow matters before you apply for a business loan. Credit decisions should always be connected to repayment ability.

Keep Business Records Organized

Good records support business credit in several ways. They help owners monitor bills, due dates, account balances, and payment history. They also make lender conversations more professional.

At minimum, owners should keep business bank statements, tax records, invoices, vendor agreements, credit card statements, and loan documents. These records can help explain the company’s financial behavior.

Organized records are especially important when applying for financing. Lenders may ask for proof of revenue, expenses, debts, and repayment ability. Clear records make those requests easier to answer.

New owners should create a simple system early. Digital folders, accounting software, and regular monthly reviews can all help. Organizations like SCORE also provide educational resources for small business owners. The best system is one the owner will actually maintain.

Avoid Trying to Build Business Credit Too Fast

Some advice makes business credit sound like a shortcut to easy financing. That can be dangerous. Credit is useful, but it is not free money.

Opening too many accounts quickly can create confusion. It can also increase the risk of missed payments. New owners should focus on accounts that serve a real purpose.

Borrowing before the business is ready can create long-term pressure. A credit line or card may feel helpful at first. If repayment becomes difficult, the same tool can weaken the business.

Responsible growth is better than fast expansion. Business credit should support the company’s progress. It should not push the owner into debt before the business can handle it.

Check Your Business Credit Profile Periodically

Once a business begins using credit, owners should review the company’s credit profile periodically. This can help identify errors, missing accounts, or unexpected negative information. It can also show whether credit-building efforts are actually being reported.

Business credit reporting is different from personal credit reporting. Not every vendor reports activity. Not every score uses the same information. Owners should avoid assuming that one report tells the whole story.

If an error appears, document the issue and follow the reporting agency’s correction process. Keep copies of statements, payment confirmations, and correspondence. Clear evidence can help support a correction request.

Periodic review also helps owners understand lender questions. If a lender sees something unexpected, the owner can respond more confidently. That confidence comes from knowing the company’s own financial record.

When Business Credit Can Help With Financing

Business credit may help when a company applies for loans, lines of credit, vendor terms, or equipment financing. It can support the lender’s view of repayment behavior. It may also help the owner qualify for better terms over time.

However, business credit is only one part of the financing picture. Lenders may also review revenue, cash flow, time in business, collateral, personal credit, and industry risk. A good credit profile cannot replace weak fundamentals.

That is why business credit should be built alongside stronger operations. Owners should focus on reliable revenue, clean records, manageable debt, and realistic planning. Those pieces work together.

For future borrowing decisions, owners may also review business loan requirements. Understanding lender expectations can help connect credit habits to real financing opportunities.

The Bottom Line on Business Credit

Business credit for new business owners is not mysterious once the pieces are separated. It begins with real accounts, clean records, timely payments, and careful financial habits. It grows as the business proves it can manage obligations.

Personal credit may still matter during the early years. That is normal for many newer companies. Over time, a responsible business credit history can give the company more financial identity of its own.

New owners should avoid shortcuts and hype. The strongest credit profile is usually built slowly and honestly. It should reflect a business that understands its bills, cash flow, and repayment responsibilities.

Good business credit is not the entire foundation of financing. It is one important part. When paired with strong records, realistic borrowing, and steady cash flow, it can help a young business become more credible.

Financial Information Disclaimer: This article is for general educational purposes only. It is not financial, legal, tax, or accounting advice. Business owners should consult qualified professionals about their specific circumstances before making financial or legal decisions.

Photo Credit: All images © Sloan Digital Publishing and licensed stock sources. Used with permission.

{kind=link}