Editor’s Note: This article has been lightly updated for clarity and readability while preserving its original small business lending guidance.

Running a small business often requires careful borrowing decisions. A loan can help a business grow, survive a slow season, buy equipment, manage cash flow, or take advantage of a new opportunity.

However, not every loan offer is helpful. Some lenders use confusing terms, rushed sales tactics, high fees, or repayment structures that can trap a business in debt. Learning how to avoid predatory lenders and bad loan terms can protect both your business and your personal financial future.

Predatory lending can be especially dangerous for newer business owners who need money quickly. When cash is tight, a fast approval may feel like a solution. But a loan that looks convenient today can become a serious burden if the true cost is hidden.

What Is Predatory Lending?

Predatory lending involves unfair, deceptive, or abusive lending practices. These practices can mislead borrowers about the real cost, risk, or repayment burden of a loan.

Some predatory lenders advertise quick cash, easy approval, or “no credit check” funding. Those promises may sound appealing, but they can come with high fees, confusing contracts, aggressive repayment terms, or automatic withdrawals that strain business cash flow.

The problem is not simply that a loan is expensive. The bigger concern is whether the borrower clearly understands the cost and has a realistic ability to repay. A business owner should never feel tricked, rushed, or pressured into signing a financing agreement.

Warning Signs of Predatory Lenders

Predatory lenders often rely on confusion and urgency. They may not explain the loan clearly, or they may make the offer sound safer than it really is.

Watch for these warning signs before signing a business loan agreement:

- No credit check required: This may sound convenient, but it can be a warning sign of very high costs or risky repayment terms.

- Confusing or unclear terms: A trustworthy lender should be able to explain the loan in plain language.

- High fees or unclear fees: Origination fees, processing fees, administrative fees, and other charges should be disclosed before you sign.

- Pressure to sign immediately: Be careful if a lender says the offer will disappear unless you act right away.

- Daily or weekly withdrawals: Frequent automatic payments can drain cash flow, especially if your business income is irregular.

- Prepayment penalties: Some loans charge extra if you pay the balance early. Always check this before signing.

- No clear APR or total cost: If the lender will not explain the full cost of borrowing, that is a serious concern.

- Blank spaces in the agreement: Never sign a contract with missing numbers, incomplete terms, or vague repayment language.

Loan Types That Require Extra Caution

Some types of business financing are not automatically predatory, but they do require careful review. The structure, cost, and repayment schedule matter just as much as the name of the product.

- Merchant cash advances: These may provide quick funding, but repayment is often tied to daily or weekly business receipts.

- Short-term business loans: These can be useful in some situations, but the repayment window may be tight.

- Loans with stacked fees: Several smaller fees can add up and make the loan much more expensive than expected.

- Automatic renewal agreements: Some contracts may renew or refinance debt in ways that add new costs.

- Loans secured by personal assets: Be especially careful if your home, vehicle, or personal savings could be at risk.

The key is not to reject every fast or short-term financing option. The key is to understand exactly what you are signing and whether the repayment terms match your business’s real cash flow.

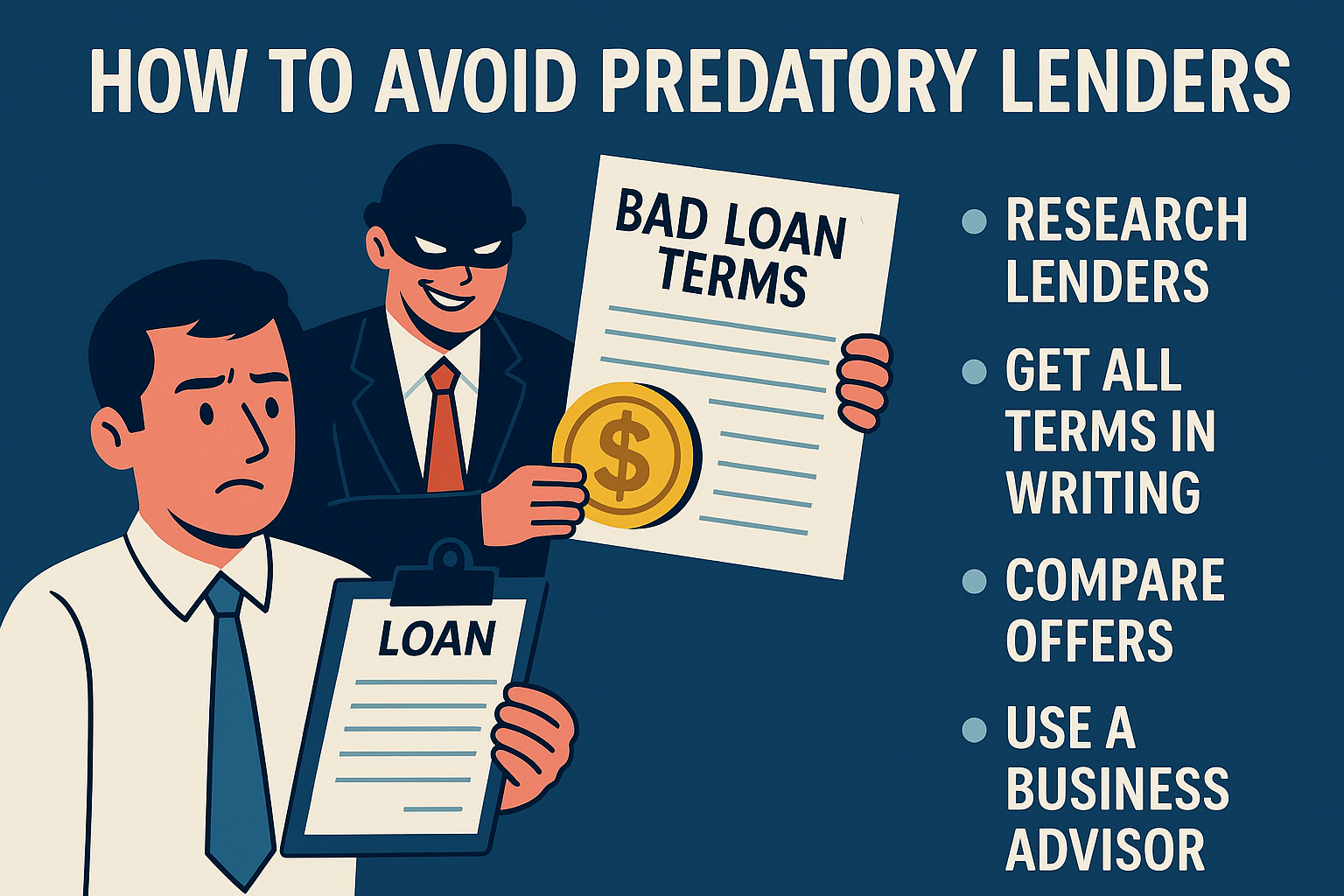

How to Protect Yourself From Bad Loan Terms

The best protection against predatory lending is preparation. Before you apply, know what your business needs, how much you can repay, and what type of financing makes sense for your situation.

- Research the lender: Look for a professional website, clear contact information, reviews, complaints, licensing information, and a track record you can verify.

- Ask for all terms in writing: Do not rely on verbal promises. The written agreement is what controls the loan.

- Request the APR or estimated annualized cost: This can help you compare offers more clearly.

- Compare more than one offer: A second or third offer can show whether the first lender’s terms are reasonable.

- Read the repayment schedule carefully: Make sure the payment timing matches your revenue cycle.

- Check for prepayment penalties: Understand whether paying early will save money or trigger an extra charge.

- Get help before signing: A small business advisor, accountant, attorney, or local SBDC counselor may spot problems you missed.

Questions to Ask Before You Sign

A responsible lender should be willing to answer basic questions clearly. If the answers are vague, rushed, or evasive, slow down before moving forward.

- What is the total repayment amount?

- What fees are included?

- What is the APR or estimated annualized cost?

- How often will payments be withdrawn?

- Can the payment amount change?

- Is there a prepayment penalty?

- Is a personal guarantee required?

- What happens if the business has a slow month?

- Will the lender report repayment activity to business credit bureaus?

- What collateral or personal assets are at risk?

These questions are not rude. They are part of responsible borrowing. A lender who discourages questions may not be the right lender for your business.

Smarter Alternatives to Predatory Lending

If a loan offer feels risky, look for safer funding options before signing. You may have more choices than you realize.

- SBA-backed loans: These loans are made by lenders and partially guaranteed by the U.S. Small Business Administration. They may offer more favorable terms for qualified borrowers.

- Microloans: Smaller loans from nonprofit or community-based lenders may include coaching or business support.

- Business lines of credit: A line of credit can provide flexible access to funds when used carefully.

- Community banks or credit unions: Local financial institutions may offer more transparent terms and relationship-based service.

- Grants: Grants are competitive and limited, but they do not have to be repaid if used properly.

- Invoice-based solutions: For businesses with unpaid invoices, certain financing options may help bridge timing gaps, but the terms still need careful review.

The U.S. Small Business Administration provides information about loan programs, including 7(a), 504, and microloan options. These programs are not right for every borrower, but they are worth reviewing before accepting a high-cost loan. Learn more from the SBA.

Why Loan Structure Is Important

A loan can look reasonable at first glance and still create problems because of its structure. Payment timing, fees, collateral, personal guarantees, and renewal terms all affect the real risk.

For example, daily withdrawals may be difficult for a business that receives most of its income once or twice a month. A short repayment period may also create pressure if the loan was used for a long-term need.

This is why business owners should look beyond the approval amount. The most important question is not only, “Can I get the money?” It is also, “Can my business repay this safely?”

What to Do If You Already Signed a Bad Loan

If you suspect you signed a bad loan agreement, do not ignore the problem. The sooner you act, the more options you may have.

- Gather the loan agreement, payment records, emails, and any marketing materials you received.

- Ask an accountant, attorney, or business advisor to review the terms.

- Contact the lender and ask whether revised repayment terms are possible.

- Explore refinancing with a reputable lender if the numbers make sense.

- Contact your state attorney general or financial regulator if you believe the lender used deceptive practices.

- Consider submitting a complaint to the Consumer Financial Protection Bureau if the issue falls within its complaint process.

The CFPB allows people to submit complaints about financial products or services and says it forwards complaints to companies for review and response when appropriate. Visit the CFPB complaint page.

Final Thoughts

Small business loans can be helpful, but only when the terms are clear, fair, and manageable. A good financing decision should support your business instead of draining it.

Predatory lenders thrive when borrowers feel rushed, confused, or desperate. Taking time to compare offers, ask questions, and read the contract can prevent expensive mistakes.

Trust your instincts. If something feels wrong, unclear, or too good to be true, slow down. Your business deserves funding that works for you, not against you.

Sources

- Consumer Financial Protection Bureau: Submit a Complaint

- U.S. Small Business Administration: Loans

- U.S. Small Business Administration: Funding Programs

- SCORE: The Requirements for a Small Business Loan

- FDIC: Predatory Lending Overview

This article is for general educational purposes only and should not be considered legal, financial, or lending advice. Business owners should review loan agreements carefully and consult a qualified professional when needed.

Photo Credit: All images © Sloan Digital Publishing and licensed stock sources. Used with permission.

{kind=link}