Talk to your lender before cash flow trouble becomes a missed payment. Many business owners wait because the conversation feels uncomfortable. That delay can make the problem harder to solve. Early communication often gives both sides more room to work.

Cash flow pressure can happen even in a real business with customers, sales, and effort. A delayed payment, slow season, large repair, tax bill, or inventory purchase can create stress. The issue may be temporary, but the lender will not know that unless the owner explains it clearly.

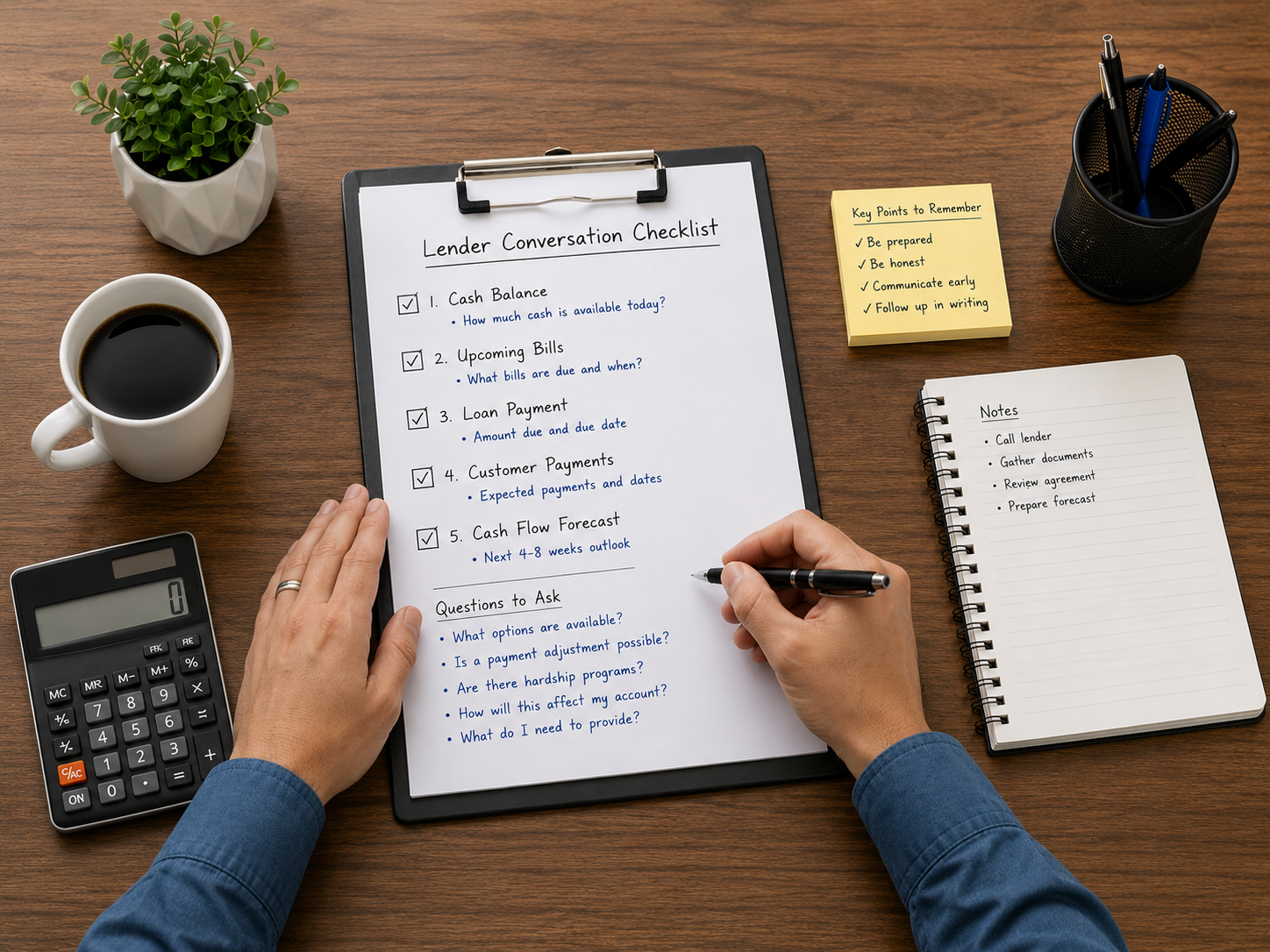

The goal is not to sound perfect. The goal is to sound prepared, honest, and serious about repayment. A calm lender conversation can help owners understand options before the situation grows worse.

Why You Should Talk to Your Lender Early

Many owners avoid difficult lender conversations until a payment is already late. That is understandable, but it can reduce available options. A lender may respond better when the owner communicates before the account becomes a problem.

Early contact shows that the owner is paying attention. It also gives the lender more time to review the situation. Silence may make the lender assume the borrower is ignoring the obligation.

Some lenders may offer a temporary adjustment, payment timing discussion, or hardship review. Others may have fewer options. Either way, the owner learns more by asking early.

For related guidance, owners may review what happens if you miss a business loan payment. Waiting until after a missed payment can make the conversation more urgent.

Know What You Need Before You Call

Before calling, owners should know what problem they are trying to solve. Is the issue one upcoming payment, several months of pressure, or a larger cash flow shortage? The answer affects the conversation.

A lender may ask whether the business can make the next payment. They may also ask when customer payments are expected. Owners should prepare realistic answers before the call.

It helps to write down the immediate concern. For example, the owner may need ten extra days, a discussion about payment timing, or clarification about available options. A clear request is easier to discuss.

Owners should avoid calling with only fear and no information. A worried call is human, but a prepared call is more useful. Preparation helps the owner stay steady.

Gather the Right Cash Flow Information

Business owners should review basic numbers before contacting the lender. This does not require perfect reports. It does require enough information to explain the problem clearly.

Start with current cash on hand. Then list upcoming bills, payroll, taxes, rent, supplier payments, and loan payments. Also list expected customer payments and when they should arrive.

A simple cash flow forecast can help. Even a one-page forecast for the next four to eight weeks may reveal the pressure point. It can show whether the problem is temporary or ongoing.

For deeper planning, owners may review why cash flow comes before a business loan application. Cash flow review helps before borrowing and during repayment.

Review the Loan Agreement First

The loan agreement controls the borrower’s obligations. Before contacting the lender, owners should review payment terms, late fees, grace periods, default language, and notice requirements. These details help frame the conversation.

The agreement may also include covenants, collateral terms, or personal guarantees. Those sections can affect what happens if payments become difficult. They should not be ignored.

Owners should mark any section they do not understand. Then they can ask the lender to explain it. Important answers should be confirmed in writing.

For related background, owners may review business loan covenants and personal guarantees on business loans. Those terms can become important during repayment stress.

Explain the Problem Clearly

When owners contact the lender, they should explain the issue without exaggeration. A clear explanation builds more trust than vague worry. The lender needs facts, timing, and context.

For example, an owner might say a large customer payment is delayed. Another may explain that seasonal revenue dropped more than expected. A third may describe an unexpected equipment repair.

The explanation should include whether the issue is temporary. If it is ongoing, the owner should say that too. Lenders do not benefit from being surprised later.

Owners should avoid blaming, guessing, or making dramatic statements. The tone should be calm and factual. The message should be that the owner is addressing the problem.

Ask Specific Questions About Options

A productive lender conversation includes questions. Owners should ask what options may exist before the account becomes late. They should also ask what happens if payment cannot be made on time.

Possible questions include whether a grace period exists. Owners can ask whether a payment date can be adjusted. They can also ask whether temporary hardship procedures are available.

Some lenders may discuss deferment, modification, catch-up plans, waivers, or short-term arrangements. These options are not guaranteed. The loan type, lender policy, and borrower history all matter.

Owners should ask how any option affects fees, credit reporting, collateral, guarantees, and future borrowing. A short-term fix should not create hidden long-term damage.

Do Not Promise More Than You Can Pay

During a stressful call, owners may feel tempted to promise too much. That can create a second problem. A promise that fails later may damage lender trust.

It is better to give a realistic payment date than an optimistic one. If the owner is unsure, that uncertainty should be stated clearly. Honest limits are safer than hopeful guesses.

Owners should also avoid agreeing to new terms too quickly. A revised agreement may include fees, waivers, new deadlines, or stronger lender rights. Those details deserve careful review.

If the proposal is complicated, professional guidance may be wise. An attorney, CPA, or business adviser can help review the terms before signing.

Follow Up in Writing

After the call, owners should send a written summary. This can be a short email confirming what was discussed. Written follow-up helps prevent confusion later.

The message should include the date of the conversation, who participated, and any next steps. It should also list documents the lender requested. If a deadline was discussed, include that too.

Owners should keep copies of every email, notice, and document sent to the lender. Good records matter when repayment problems arise. They also help advisers understand the situation later.

Verbal reassurance is not enough for major repayment issues. If the lender offers an arrangement, ask for the terms in writing. The written version should match the conversation.

When to Bring in Professional Help

Some cash flow problems are simple timing issues. Others may involve deeper financial risk. Owners should know when they need help beyond a lender phone call.

A CPA can help review cash flow, taxes, financial statements, and repayment ability. A bookkeeper can organize receivables, payables, and upcoming bills. An attorney can review default terms, collateral rights, or personal guarantees.

A business adviser may help owners prepare for the lender conversation. Support organizations like SCORE offer educational mentoring and planning resources. The Small Business Administration also provides general loan information.

Getting help does not mean the owner failed. It means the situation deserves careful handling. Early guidance may prevent a temporary issue from becoming a serious one.

What Not to Do When Cash Flow Gets Tight

Owners should not ignore lender notices. They should not assume the lender already understands the problem. They should not wait until several payments are late.

It is also risky to borrow blindly from another source. New debt may cover one payment while creating more pressure later. Fast financing can be expensive and difficult to manage.

Owners should avoid hiding information from key advisers. A CPA, bookkeeper, or attorney can only help with accurate facts. Delayed honesty can limit useful options.

For related guidance, owners may review how to compare business loan offers before you sign. New financing should always be reviewed carefully.

How to Prevent the Same Problem Again

After the immediate issue improves, owners should review what caused the pressure. A one-time problem may need a simple adjustment. A repeating problem may require deeper changes.

Cash flow forecasting can help owners see trouble earlier. A weekly review of deposits, bills, payroll, taxes, and loan payments can reveal gaps before due dates arrive. That gives owners more time to respond.

Owners may also need stronger collection habits. Late customer payments can strain even profitable businesses. Clear invoices, follow-up routines, and payment terms can improve timing.

A modest reserve can also help. It may not solve every problem, but it can reduce stress during slow weeks. Even small reserves can protect payment consistency.

The Bottom Line When You Talk to Your Lender

Talk to your lender early when cash flow gets tight. A difficult conversation handled early is usually better than silence. Lenders may have more options before the problem grows.

Owners should gather facts, review the agreement, explain the issue clearly, and ask direct questions. They should avoid promises they cannot keep. They should also confirm important details in writing.

Cash flow stress does not automatically mean failure. It does mean the business needs attention and a practical plan. Calm communication can protect trust and preserve more choices.

The goal is not only to get through one hard month. The goal is to understand the pressure, respond responsibly, and reduce the chance of repeated trouble. That is how business owners protect both the loan relationship and the company.

Financial Information Disclaimer: This article is for general educational purposes only. It is not financial, legal, tax, or accounting advice. Business owners should consult qualified professionals about their specific circumstances before making financial or legal decisions.

Photo Credit: All images © Sloan Digital Publishing and licensed stock sources. Used with permission.

{kind=link}