Business loan requirements can feel overwhelming when you are preparing to borrow for the first time. Lenders may ask for records, credit history, revenue details, cash flow information, and repayment plans. Some may also ask about collateral or personal guarantees. The process feels easier when owners understand what lenders usually want to see.

Most lenders are trying to answer one basic question. Can this business repay the loan on time? Everything they request usually connects to that concern. Your documents, credit, revenue, and cash flow all help tell that story.

Requirements can vary by lender, loan type, industry, and business age. A bank term loan may require more documentation than a small line of credit. An SBA-backed loan may involve additional forms and eligibility rules. Still, many lenders review the same core areas before approving financing.

Why Business Loan Requirements Vary

No single checklist applies to every loan. A startup seeking its first loan is different from an established company refinancing equipment. A seasonal business is different from a company with steady monthly revenue. Lenders adjust requirements based on risk.

Loan purpose also affects the review. Equipment financing may focus on the equipment value and the business’s ability to pay. Working capital loans may focus more heavily on cash flow. Real estate or expansion loans may require deeper financial review.

Lender type also plays a role. Banks, credit unions, online lenders, community lenders, and SBA lenders may use different standards. Some lenders move quickly but charge more. Others take longer but may offer stronger terms.

Business owners should not assume one denial means every lender will say no. It may mean the business needs a different product, stronger records, or more time. Understanding the requirements helps owners apply more strategically.

Credit History Is Often Reviewed First

Credit is one of the first areas many lenders review. For newer businesses, personal credit can carry extra weight. The business may not yet have enough credit history of its own. That makes the owner’s credit profile more important.

Lenders may look for timely payments, current debt levels, recent credit activity, and serious negative marks. A strong score does not guarantee approval. However, weak credit can limit options or increase costs.

Business credit may also be reviewed if the company has established accounts. Vendor accounts, business credit cards, and prior loans may influence the lender’s view. Payment history can help show whether the company handles obligations responsibly.

Owners should review credit before applying. Errors, high balances, and recent late payments can weaken an application. Checking early gives owners time to correct problems or prepare explanations.

For related guidance, owners may review what new business owners should know about business credit. Credit preparation often starts before a loan application begins.

Cash Flow Shows Repayment Ability

Cash flow is one of the strongest parts of a business loan review. Revenue tells lenders how much money comes in. Cash flow shows whether enough money remains after expenses. That difference is important.

A business may have healthy sales but still struggle with payments. Rent, payroll, inventory, insurance, taxes, and supplier costs can reduce available cash quickly. Lenders want to know whether loan payments fit the business’s normal pattern.

Owners should review monthly cash flow before applying. Look at strong months, weak months, and seasonal changes. A payment that works during a busy season may become stressful later.

Lenders may request bank statements, financial reports, or cash flow projections. These documents help them judge repayment ability. They also help owners decide whether borrowing is wise right now.

For a deeper look at this issue, owners may later review why cash flow matters before you apply for a business loan. Repayment strength is central to responsible borrowing.

Revenue History Helps Lenders Measure Stability

Revenue history helps lenders understand the size and stability of the business. An established company with steady deposits may appear less risky. A newer business may need stronger projections, owner investment, or supporting records.

Lenders may review monthly sales, annual revenue, and growth trends. They may also compare revenue to expenses and existing debt. Large sales numbers are less useful if little money remains after costs.

Some lenders have minimum revenue requirements. Others focus more on cash flow, collateral, or the owner’s credit. Requirements can differ widely, so owners should ask before applying.

New business owners should avoid overstating revenue or relying on hopeful projections. Realistic numbers build credibility. Lenders usually prefer careful estimates over unsupported optimism.

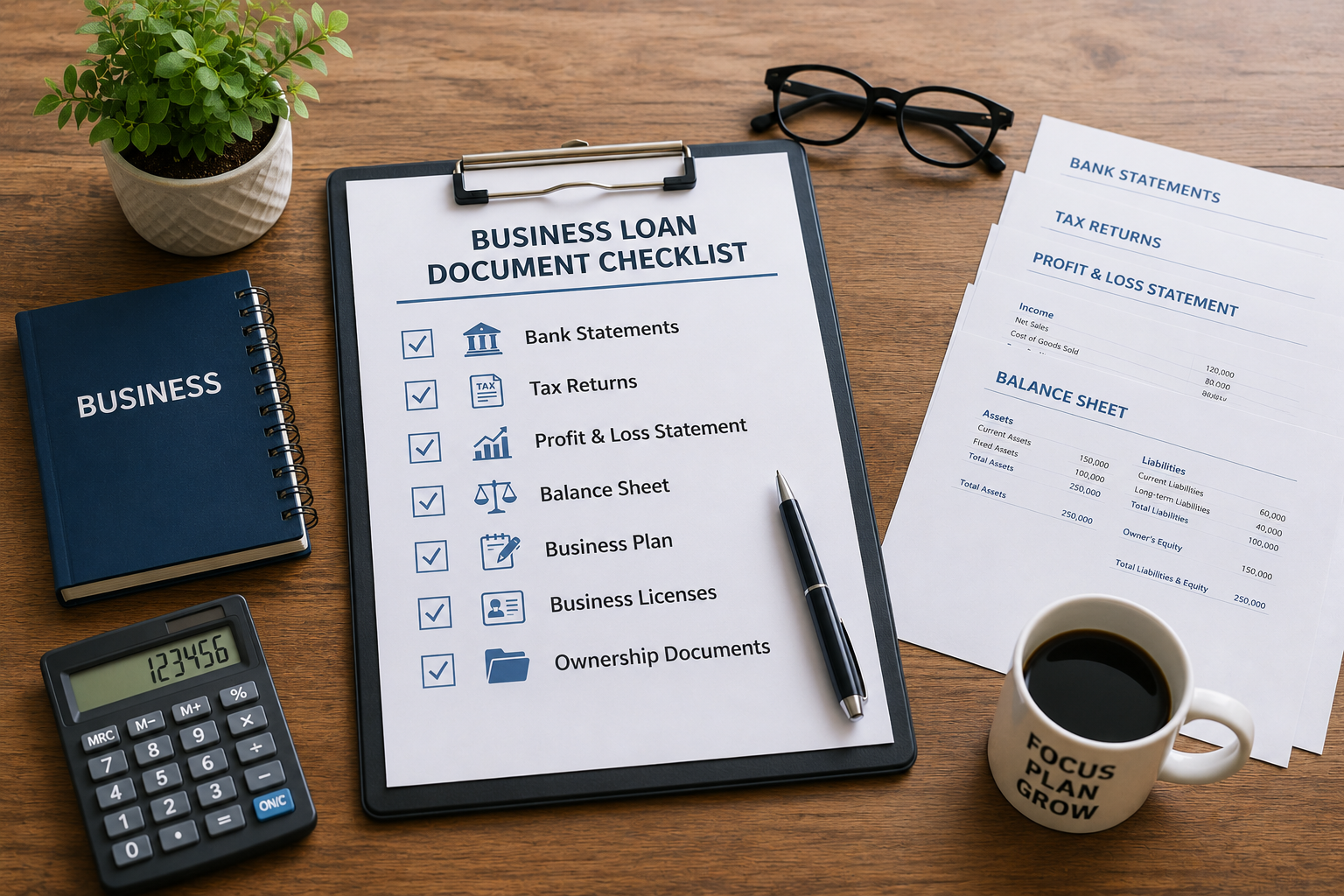

Business Loan Documents Should Be Organized Early

Loan applications often slow down when documents are incomplete. Preparing early helps owners respond quickly and professionally. It also reduces stress during the review process.

Common business loan documents may include bank statements, tax returns, profit and loss statements, balance sheets, business licenses, leases, and ownership records. Some lenders may ask for accounts receivable reports, debt schedules, or insurance information.

Startups may need a business plan and financial projections. Support organizations like SCORE provide educational resources for business planning and owner preparation. A clear plan can help explain how the loan will support the business.

Owners should create one organized loan folder before applying. Use clear file names and dates. Keep digital copies in a secure location. If a lender asks for an updated document, it should be easy to find.

A Clear Loan Purpose Helps the Application

Lenders usually want to know how the money will be used. A clear loan purpose shows planning and discipline. It also helps match the borrower with the right financing product.

Common loan purposes include equipment, inventory, working capital, expansion, renovations, marketing, or refinancing. Each purpose may call for a different structure. A long-term purchase may not fit a short repayment schedule.

Owners should be specific. Instead of saying the business needs money, explain the exact use. Include estimated costs, timing, and expected business benefit. This helps the lender understand the request.

A clear purpose also protects the owner. It reduces the chance of borrowing more than needed. It also helps avoid using debt to cover deeper problems that require a different solution.

Debt and Existing Obligations Are Reviewed

Lenders do not look at a new loan in isolation. They usually review existing debt and regular obligations. This helps them understand whether the business can handle another payment.

Existing debt may include credit cards, equipment loans, lines of credit, merchant cash advances, leases, or personal obligations tied to the business. Some debts may carry higher risk than others. Short repayment terms can be especially demanding.

Owners should prepare a debt schedule before applying. List each debt, balance, payment, interest rate, and maturity date. This gives both the lender and owner a clearer picture.

A business with heavy debt may still qualify for financing. However, the lender may request stronger cash flow, collateral, or owner support. In some cases, reducing debt first may improve future options.

Collateral and Guarantees May Be Required

Some loans require collateral. Collateral is property or business equipment that can help secure the loan. It may include vehicles, equipment, inventory, real estate, or other assets.

Collateral reduces lender risk, but it also creates owner risk. If the loan defaults, the lender may have rights related to the pledged asset. Owners should understand those terms before signing.

Some lenders may also require a personal guarantee. This means the owner may be personally responsible if the business cannot repay. Personal guarantees are common for many small business loans.

Newer owners should read guarantee and collateral language carefully. A loan can affect both the business and personal finances. Legal or financial guidance may be wise before agreeing to major obligations.

Time in Business Can Affect Approval

Time in business is another common requirement. Many lenders prefer companies with an operating history. A longer history gives them more information about revenue, expenses, and repayment ability.

Startups may face stricter review because they have fewer records. Lenders may rely more heavily on personal credit, owner experience, collateral, projections, or outside income. Some lenders may not fund very new businesses at all.

This does not mean new businesses have no options. SBA-backed loans, microloans, community lenders, and nonprofit programs may serve some younger companies. The Small Business Administration offers information about SBA loan programs and lender connections.

Owners should ask about time-in-business requirements before applying. This can prevent wasted applications. It can also help owners choose lenders that fit their stage.

Industry and Business Risk May Influence the Decision

Lenders may consider the industry when reviewing an application. Some industries have stable demand and predictable revenue. Others face heavy regulation, seasonal swings, or higher failure rates.

Industry risk does not automatically prevent approval. It may affect documentation, pricing, collateral, or required experience. Lenders may want to see that the owner understands the specific challenges.

Owners can prepare by explaining their market clearly. They should know their customers, competition, pricing, and revenue pattern. A practical explanation can help reduce uncertainty.

For newer owners, industry experience can be valuable. It shows that the owner understands daily operations. It may also help support projections and repayment plans.

Financial Statements Should Tell a Consistent Story

Financial statements help lenders understand how the business performs. A profit and loss statement shows income and expenses. A balance sheet shows assets, liabilities, and owner equity. Bank statements show actual cash movement.

These records should be consistent. If tax returns, bank deposits, and financial reports tell different stories, questions may arise. Some differences are explainable, but major gaps can slow approval.

Owners should review records before submitting an application. A CPA or bookkeeper can help correct errors and prepare clearer statements. This step is especially helpful for owners who handle bookkeeping themselves.

Clean records do not need to be perfect. They do need to be understandable. A lender should be able to follow the business’s financial picture without confusion.

Business Loan Requirements Are Also About Fit

Requirements are not just lender hurdles. They help determine whether the loan fits the business. A loan that is too large, too expensive, or too fast can create pressure.

Owners should compare payment terms, interest rates, fees, collateral, guarantees, and repayment schedules. The easiest approval may not be the best option. A slower lender may offer better terms.

Borrowers should also consider timing. A business may qualify for a smaller loan now but a stronger loan later. Waiting can be wise if revenue, records, or credit will improve soon.

For first-time borrowers, preparation can be more valuable than speed. A thoughtful application can help owners avoid poor financing choices. It can also lead to more productive lender conversations.

How to Prepare Before Contacting a Lender

Before contacting a lender, owners should review the main business loan requirements. Start with credit, cash flow, revenue, documents, debt, and loan purpose. These areas usually shape the conversation.

Next, organize recent bank statements, tax returns, financial reports, and ownership documents. Prepare a short explanation of the loan request. Include the amount, purpose, expected benefit, and repayment plan.

Owners should also decide what questions to ask the lender. Ask about minimum credit, revenue, time in business, collateral, fees, and timeline. This helps avoid unnecessary applications.

For a broader preparation guide, owners may review how to prepare before applying for your first small business loan. Strong preparation can make lender discussions more useful.

The Bottom Line on Business Loan Requirements

Business loan requirements are easier to understand when you see what lenders are really evaluating. They want to know whether the business can repay, whether records support the request, and whether the loan fits the borrower.

Credit, cash flow, revenue, documents, debt, collateral, and time in business all help answer those questions. A newer business may need more preparation because it has less history. That does not make approval impossible.

The best approach is to prepare before pressure builds. Review your records, understand your numbers, and define your loan purpose clearly. Ask lenders what they require before starting a formal application.

Good preparation does more than improve approval chances. It helps business owners make wiser borrowing decisions. That is the real value of understanding business loan requirements before applying.

Financial Information Disclaimer: This article is for general educational purposes only. It is not financial, legal, tax, or accounting advice. Business owners should consult qualified professionals about their specific circumstances before making financial or legal decisions.

Photo Credit: All images © Sloan Digital Publishing and licensed stock sources. Used with permission.

{kind=link}