How to Avoid Predatory Lenders and Bad Loan Terms

Running a small business requires careful financial planning. Many entrepreneurs turn to loans for growth, survival, or stability. While borrowing money can help your business thrive, it can also lead to trouble if the lender is not trustworthy. Predatory lenders target small businesses with deceptive or unfair practices that often result in debt traps. Understanding how to recognize and avoid these predatory lenders can protect your business and personal financial future.

What Is Predatory Lending?

Predatory lending involves unethical practices that mislead borrowers. These lenders often disguise the true cost of a loan. They might advertise quick cash or guaranteed approval but hide high fees, confusing terms, or automatic withdrawal requirements. The result is often unmanageable debt, especially for vulnerable or first-time business owners. Predatory lending is not just bad business—it can lead to bankruptcy or the closure of a once-thriving company.

Warning Signs of Predatory Lenders

Here are common red flags that may indicate a predatory lender:

- No credit check required: While this may seem convenient, it often signals hidden costs or high risk for borrowers.

- Confusing or unclear terms: Predatory lenders avoid plain language to hide their true intentions. Contracts may be vague or contradictory.

- Excessive fees and interest rates: Some lenders charge interest rates above 100% or add fees that aren’t disclosed upfront.

- High-pressure sales tactics: You may be told to sign now or lose the offer. Reputable lenders never rush borrowers.

- Frequent, automatic repayments: Daily or weekly withdrawals can drain your bank account and leave you short on payroll or expenses.

- Prepayment penalties: Good loans allow early payment. Predatory loans penalize you for paying off your balance sooner.

- Lack of transparency about APR: The annual percentage rate should include all costs. If it’s hidden or unclear, that’s a serious red flag.

Types of Loans Often Linked to Predatory Lending

Some loan types are more commonly associated with predatory behavior. Use extra caution when considering the following:

- Merchant Cash Advances (MCAs): These offer quick funding but require daily or weekly repayments, often with triple-digit effective APRs.

- Payday-style business loans: These are short-term loans with lump-sum repayments and extremely high costs.

- Loans with excessive fees: Some lenders add origination, documentation, or administrative fees that greatly increase the cost.

- Loans with automatic renewals: If you miss a payment, some loans renew automatically with new fees and terms.

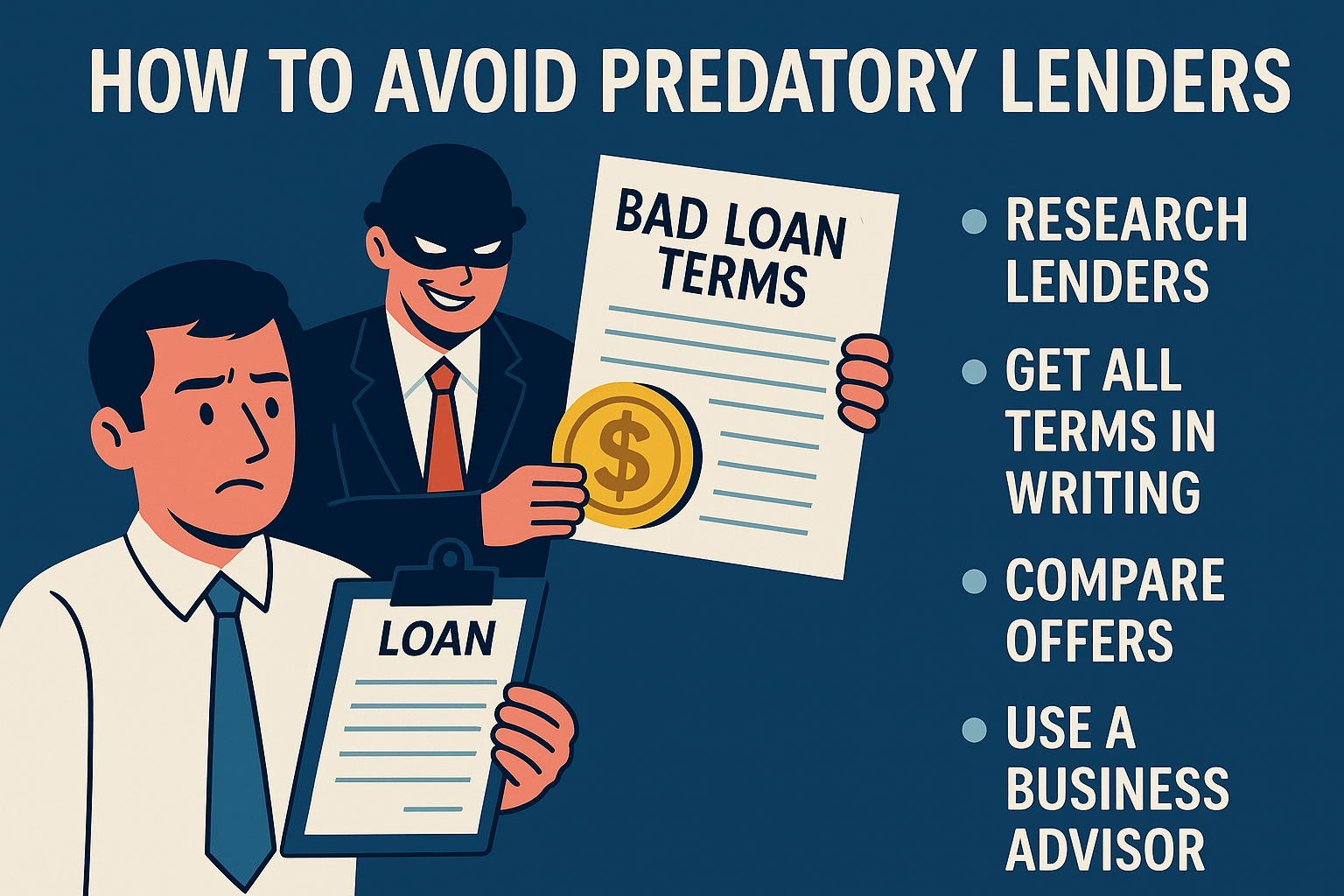

How to Protect Yourself From Bad Loan Terms

The best defense against predatory lending is education and preparation. Use these steps to safeguard your business:

- Research lenders thoroughly: Look for reviews, Better Business Bureau ratings, and complaints through the CFPB database.

- Ask for all terms in writing: Never rely on verbal promises. Always read the entire loan contract before signing.

- Demand transparency about APR: This figure includes interest and fees. If a lender refuses to provide it, walk away.

- Compare multiple loan offers: Shop around to get a sense of fair rates and flexible repayment options.

- Use a business advisor or attorney: Professionals can spot predatory terms you might miss. Many local SBDCs offer free help.

- Choose appropriate repayment structures: Loans should match your income cycle. Avoid daily withdrawals if your revenue is monthly.

- Check for prepayment penalties: Ensure you’re allowed to pay early without a fee.

Smarter Alternatives to Predatory Lending

Fortunately, there are safer ways to access funding for your business. Consider these responsible alternatives:

- SBA Loans: Backed by the U.S. Small Business Administration, these offer low rates and longer repayment terms.

- Microloans: These are smaller loans from nonprofit or community lenders with fair rates and coaching support.

- Business lines of credit: These give you flexible access to funds when needed, with interest charged only on what you use.

- Grants: These are non-repayable funds offered by government or private entities. They may be competitive but worth exploring.

- Crowdfunding: Platforms like Kickstarter or GoFundMe allow businesses to raise funds from supporters without taking on debt.

Why Loan Structure Matters

Even if a loan looks reasonable at first glance, the structure can make it dangerous. For example, a short repayment window paired with daily deductions can destabilize your cash flow. Some lenders also use confusing language that hides the true cost. That’s why reading the full contract and understanding your repayment obligations is so important.

What to Do If You’ve Already Signed a Bad Loan

If you suspect you’re in a predatory loan agreement, take action quickly:

- Consult with a financial advisor or attorney to review your options.

- Reach out to your lender to renegotiate terms or request deferment if your cash flow is unstable.

- Contact the Consumer Financial Protection Bureau to file a complaint.

- Explore refinancing with a reputable lender who can consolidate your debt under better terms.

Final Thoughts

Small business loans can be helpful, but only if they come from fair and transparent lenders. Predatory lenders thrive on confusion, pressure, and desperation. Taking time to research and compare offers is one of the best ways to protect yourself. Trust your instincts—if something seems off, it probably is. Your business deserves funding that works for you, not against you.

{kind=link}