Miss a business loan payment, and the situation can feel stressful quickly. A missed payment may bring fees, lender calls, or concern about default. It can also raise questions about cash flow, collateral, personal guarantees, and future borrowing. The best response is usually calm review, not panic.

Every loan agreement is different. One lender may allow a short grace period. Another may charge a fee immediately. Some loans may define default after one missed payment, while others follow a longer process. Owners should check the written agreement before assuming what happens next.

A missed payment should never be ignored. Early communication can sometimes preserve options and reduce lender concern. The goal is to understand the problem, contact the lender, and avoid repeated payment trouble.

If you miss a business loan payment, the smartest first step is to review the agreement before making assumptions.

What Happens If You Miss a Business Loan Payment?

The first consequence usually depends on the loan agreement. The lender may charge a late fee, send a notice, contact the borrower, or apply default terms. The timing can vary by lender and loan type.

Some lenders treat one late payment as a warning sign. Others may respond more seriously, especially if the account already has problems. A missed payment can also affect automatic withdrawals, account standing, and borrower trust.

Business owners should review the payment section first. Look for grace periods, late fees, default language, and notice requirements. These details explain what the lender may do next.

For broader repayment planning, owners may review why cash flow comes before a business loan application. Strong cash flow review can reduce payment surprises later.

When You Miss a Business Loan Payment, Default May Not Start Immediately

A late payment and a loan default are related, but they are not always identical. A payment may be late before the lender officially declares default. The agreement controls that distinction.

Some loans include a grace period. During that time, the borrower may still make the payment before stronger consequences begin. Other loans may charge a late fee immediately, even if default comes later.

Default language deserves careful attention. It may include missed payments, covenant breaches, insurance lapses, false information, or unauthorized debt. A business may default without missing a payment if another obligation is broken.

Owners should never guess about default rules. They should read the agreement and ask the lender for clarification. If the language is serious or confusing, professional guidance may be wise.

Review the Loan Agreement First

The written loan agreement controls the borrower’s obligations. Emails, sales calls, and verbal explanations may help, but the signed documents usually control. That is why owners should review them carefully after a missed payment.

Start with the payment terms. Check the due date, payment amount, payment method, grace period, late fee, and default section. Also review whether the lender can change rates, fees, or payment methods after problems occur.

Next, check any collateral, guarantee, or covenant sections. A missed payment can connect to other parts of the agreement. The lender may have rights that go beyond collecting the overdue amount.

For related preparation, owners may review business loan requirements. Understanding lender expectations before borrowing can make repayment terms easier to follow.

Contact the Lender Early

Silence rarely helps after a missed payment. Lenders may view no communication as a warning sign. Early contact can show that the owner is paying attention and wants to resolve the problem.

Owners should explain the issue clearly. Was the payment missed because of a temporary cash shortfall, bank error, delayed customer payment, or unexpected expense? The reason may affect the conversation.

Before calling, gather basic information. Know the missed amount, expected payment date, current cash position, and whether future payments may also be difficult. Clear information makes the discussion more productive.

A lender may offer options, but not always. Possible options may include catching up quickly, adjusting payment timing, discussing a waiver, or reviewing hardship procedures. The agreement and lender policy will guide what is possible.

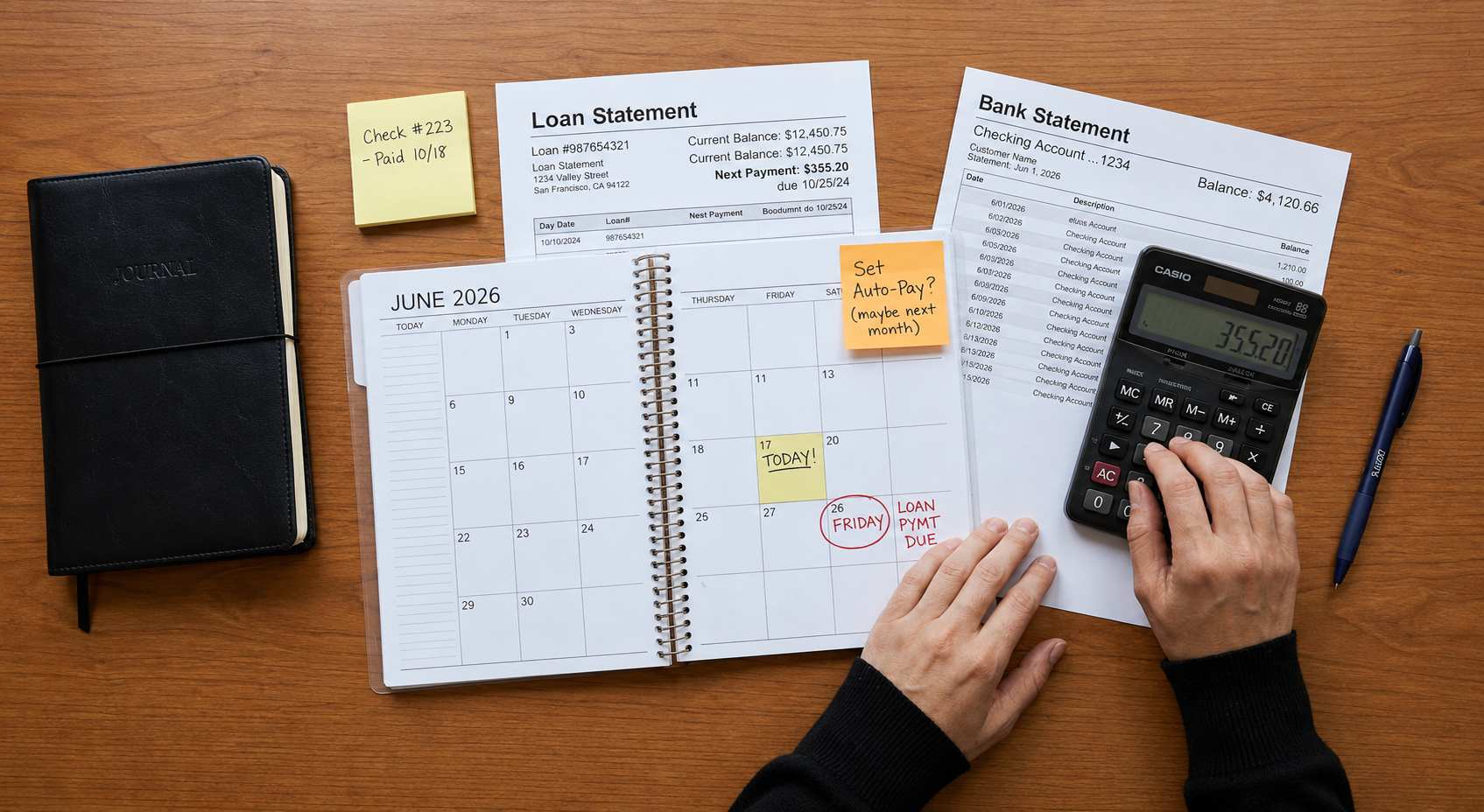

Late Fees and Extra Costs Can Add Up

A missed payment may trigger late fees. Some loans charge a flat fee. Others charge a percentage of the missed amount. Short-term products may include different cost structures.

Fees can make a difficult month worse. A business already short on cash may struggle more once penalties appear. Owners should ask for the exact amount needed to bring the loan current.

Late costs may also include returned-payment fees, bank fees, collection costs, or default interest. These charges depend on the loan documents. They should not be assumed or ignored.

Owners should ask the lender to explain the balance in writing. A clear payoff or catch-up amount helps prevent confusion. It also helps the owner plan the next step.

Credit Reporting May Be Affected

A missed business loan payment may affect credit reporting, depending on the lender and loan type. Some lenders report to business credit bureaus. Others may report certain problems to personal credit bureaus, especially if a personal guarantee exists.

Owners should ask how the lender reports late payments. They should also ask when reporting begins. A payment that is a few days late may not be treated the same as one that remains unpaid for longer.

Credit damage can affect future borrowing. It may also affect vendor terms, insurance reviews, or business credit access. The effect depends on the reporting system and the borrower’s overall history.

For related background, owners may review what new business owners should know about business credit. Good credit habits can support future financing options.

Personal Guarantees Can Increase the Risk

If the owner signed a personal guarantee, a missed payment can become more serious. The loan may belong to the business, but the guarantee may create personal repayment responsibility. That risk depends on the written terms.

One missed payment may not immediately lead to personal collection. However, it can start a process that eventually affects the guarantor. Owners should know when the lender can pursue personal responsibility.

Guarantee language can be broad or limited. It may cover principal, interest, fees, collection costs, renewals, or future obligations. These details should be reviewed before payment problems grow.

For more guidance, owners may review personal guarantees on business loans. A guarantee should never be treated as harmless fine print.

Collateral May Also Be Involved

Some business loans are secured by collateral. Collateral may include equipment, vehicles, inventory, receivables, real estate, or broader business assets. A missed payment may raise concern about those pledged assets.

The lender may not immediately take action against collateral. Still, the loan agreement may give the lender rights after default. Owners should understand those rights before the situation worsens.

Collateral issues can also affect business operations. Losing access to key equipment or receivables can create deeper cash flow problems. That is why secured loans deserve careful attention.

Owners should ask what assets secure the loan and what steps happen after missed payments. A written explanation is better than assumptions.

Covenants Can Make Payment Trouble Worse

Some loans include covenants. These are promises or restrictions written into the agreement. A missed payment may occur alongside a covenant problem, especially when cash flow is already weak.

For example, the business may miss a payment and also fall below a required financial ratio. It may fail to provide reports on time. It may take on extra debt without lender approval.

Multiple problems can give the lender more concern. They may also reduce the owner’s options. Tracking covenants helps owners identify trouble before it grows.

For related guidance, owners may review business loan covenants. Covenant compliance can matter even when payments are usually made on time.

Do Not Borrow Blindly to Cover the Payment

Some owners feel tempted to borrow quickly after missing a payment. That may solve the immediate problem, but it can create a larger one. Fast financing can add new payments, fees, and pressure.

Borrowing to catch up may make sense in limited situations. It may help when the shortfall is temporary and repayment is realistic. It becomes risky when the business already cannot support current debt.

Owners should review why the payment was missed. Was it a one-time timing issue, or part of a repeated cash flow pattern? The answer should guide the next move.

Before adding more debt, owners should compare the full cost and repayment schedule. For related guidance, review how to compare business loan offers before you sign.

When to Get Professional Help

Professional guidance can help when the missed payment is not easily fixed. A CPA can review cash flow, taxes, records, and repayment ability. A bookkeeper can help organize payables, receivables, and current obligations.

An attorney may be useful if default, collateral, collection, or personal guarantees are involved. Legal guidance is especially important before signing any revised agreement. Owners should understand new terms before agreeing.

A business adviser may help owners evaluate whether the problem is temporary or structural. Support organizations like SCORE offer educational business guidance. Owners can also review general loan resources from the Small Business Administration.

Getting help does not mean the owner has failed. It means the issue deserves careful review. Early guidance can prevent a small problem from becoming a larger one.

How to Prevent Repeated Missed Payments

After the immediate issue is addressed, owners should look for the cause. Repeated missed payments usually point to a deeper problem. Cash flow timing, weak margins, poor collections, or excess debt may be involved.

A simple payment calendar can help prevent avoidable mistakes. Include due dates, automatic withdrawals, bank balance checks, tax deadlines, and payroll periods. Review the calendar weekly.

Owners should also maintain a cash reserve when possible. Even a modest reserve can reduce stress during slow weeks. It can also prevent one delayed customer payment from creating a loan problem.

Regular cash flow forecasting is useful. A forecast can show payment pressure before the due date arrives. That gives owners more time to respond.

The Bottom Line If You Miss a Business Loan Payment

Miss a business loan payment, and the next step should be calm action. Review the agreement, check fees and default terms, and contact the lender early. Do not ignore notices or hope the issue disappears.

A missed payment is serious, but it does not always mean disaster. The outcome depends on the agreement, lender policy, borrower history, and how quickly the owner responds. Early communication can help preserve options.

Business owners should also review cash flow, guarantees, collateral, covenants, and future payment risk. If the issue is bigger than one late payment, professional guidance may be wise.

The goal is not just to catch up once. The goal is to understand why the payment was missed and prevent repeated trouble. That response can protect the business more than panic ever will.

Financial Information Disclaimer: This article is for general educational purposes only. It is not financial, legal, tax, or accounting advice. Business owners should consult qualified professionals about their specific circumstances before making financial or legal decisions.

Photo Credit: All images © Sloan Digital Publishing and licensed stock sources. Used with permission.

{kind=link}